Real Estate Market Intelligence April 2025

Real Estate Market Intelligence April 2025

April has proven to be one of the most volatile months of the decade (even surpassing the pandemic). Lots of unpack this month as we have the surprising lower Canadian inflation, followed by the latest Bank of Canada rate announcement, and all eyes on the federal election coming up. Let's jump right in.

Firstly, a continuation of widespread global uncertainty around tariff news is causing mental fatigue amongst many Canadian, and this has certainly trickled down to the Vancouver real estate market. Last month, Vancouver sales were down a whopping -36.8% below the 10 year average, while total inventory has shot up +44.9% above the 10 year average. To put the low sales into perspective, last month's sales were the second lowest March sales (first was in 2019) dated back in 2005. Digging deeper, between the aforementioned sales and total inventory, we're looking an a spread of a 81.7% deviation from the 10 year average, which again is at the second highest polarized market for past 25 years. In short, Buyers have "uncertainty overload", and many are taking a step back to wait this out. In such time when the volatility index is at a record high, just how do most Canadian's make sense in going out to make one of life's biggest purchases (i.e real estate)? On the other hand, Buyers who are a bit of a contrarian (or simply optimists) are now having one of best times to negotiate since 2019. With boots on the ground, I personally felt March and April were indeed two of the slowest months in recent memory. For the past two weeks, it does seem like the there is increased activity, both in terms of open house traffic with listings having offers, and that is in line with the seasonality that Spring is the busiest real estate market. Having said that, one week doesn't make a trend, but it certainly gave me the impression that Buyers are either waiting for the right chance (i.e market showings signs of bottoming), or for the ideal product (i.e entry level or competitively priced home with minimal renovations).

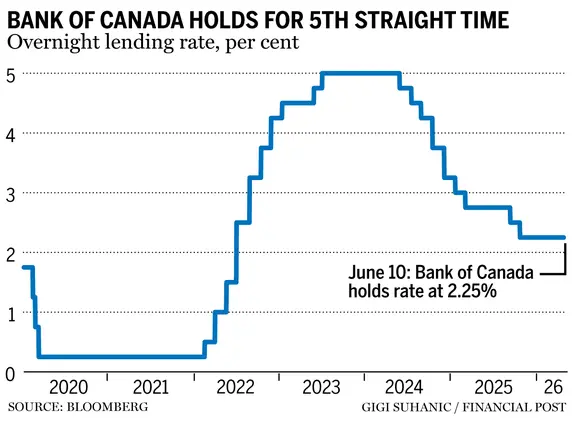

On the economic front, Canada's inflation took a surprising dip to 2.3% in March (down from 2.6% in February), and this was mainly due to lower gas prices (-1.6% year-over-year) and lower airfare prices (-4.7% year-over-year). However, food prices shot up +3.2%. Overall, the data may point out that in the time of economic uncertainty, Canadian households are adjusting their spending habits by reducing traveling and vacations just to be able to afford putting food on the table. Along the lines of keeping inflation in check, the Bank of Canada's latest announcement of holding the overnight rates may came as a surprise to some, even though I do believe this was a right move; in the face of extreme uncertainty, it may be best to stay put for now in an attempt to avoid inflation running rampant in a weaker Canadian economy. As for Canadian mortgages, the 5 year rates (mirrors that of the 5-year bond yield) jumped up 20 bps (or +0.20%) between April 4 - 11, and thus so the short-lived the talks of lower fixed rates prior to that. As most Canadian Buyers see lower borrowing rates on the horizon, they may elect to go with the variable rates. As for those who prefer more clarity with fixed payments, keep a close eye on fixed rates with the option to lock anything that's sub 4%.

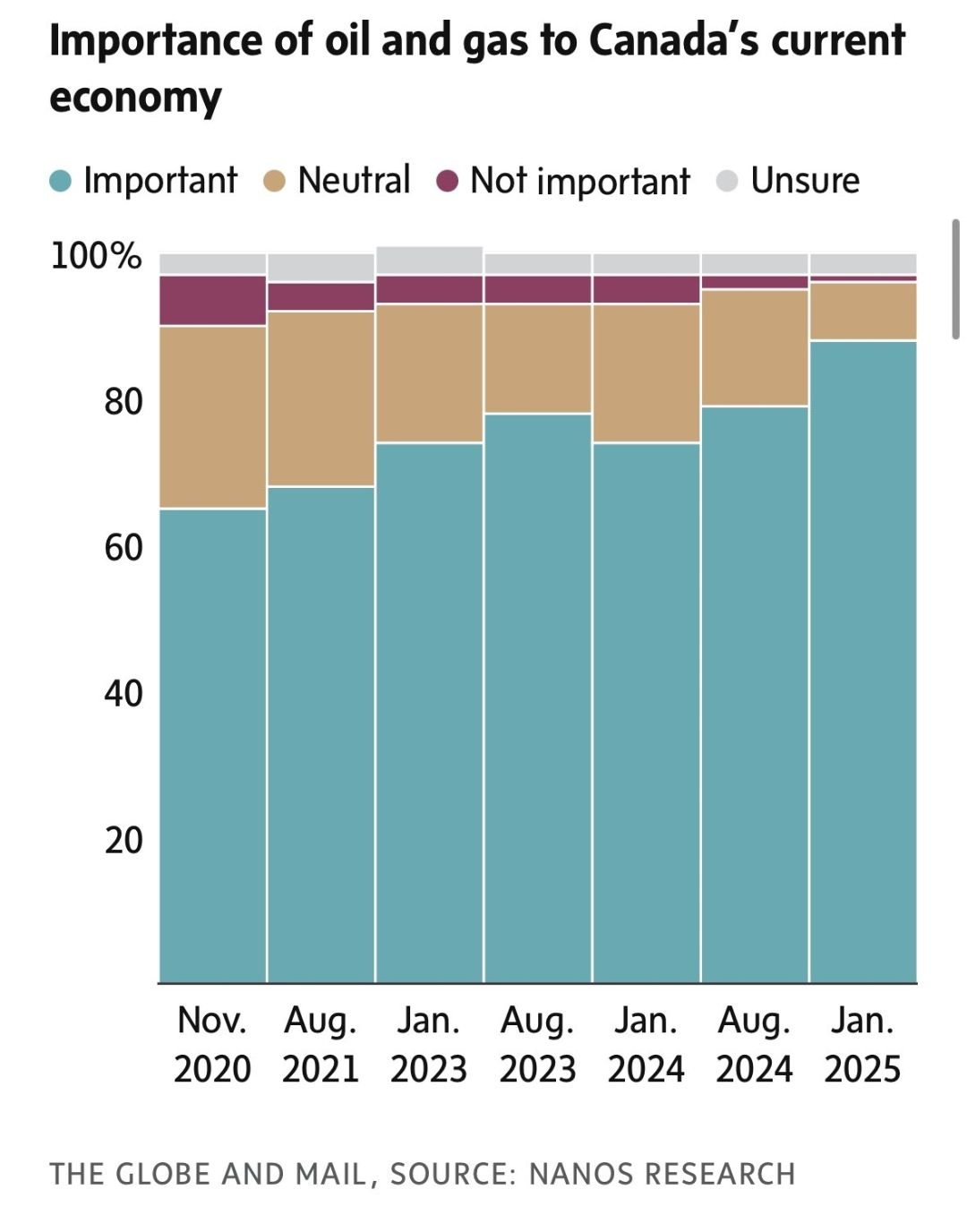

Lastly but most importantly, the Canadian federal election looms large on April 28th. This may well be the most important election in a long time. Canada is in dire need of a leader who can navigate through the financial turmoil, and reposition Canada on a global stage. Just how do we deal with the consistently low productively rate in Canada? Would Canada be able to finally unlock its most value asset, its oil and energy, to save the economy? While the world's energy consumption continue to climb to a record highs, would Canada be still on the trajectory of a greener path by capping oil production, or would Canada finally come out on top and be a global provider in energy? Whether we like it or not, change is coming. And it's long overdue. Next month, Canada will have a new leader. Let's see.

Some of the unique trends I've been observing:

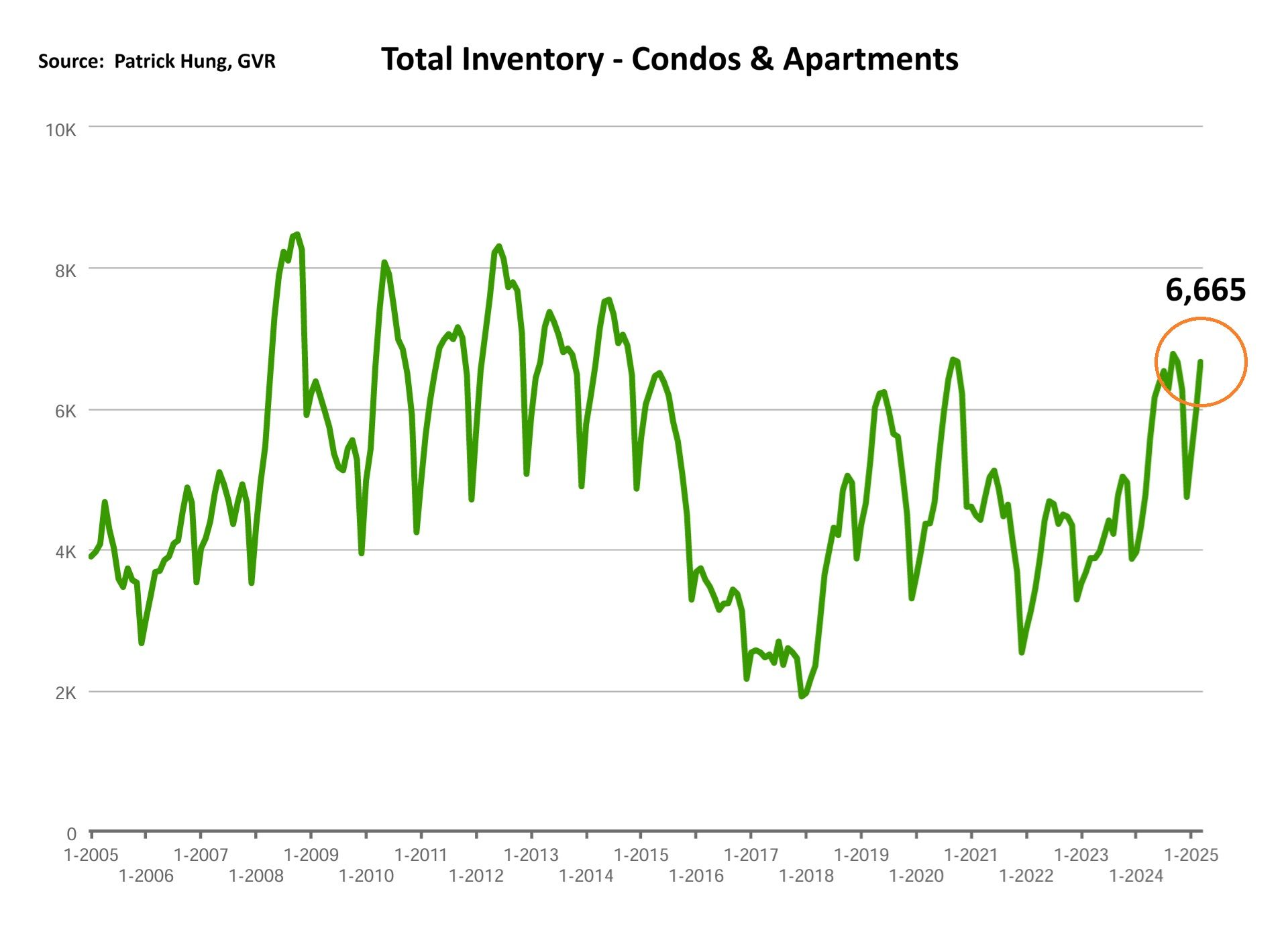

1. Bank of Canada doesn't have to worry about shelter inflation anymore (which is included in the inflation data). The Canadian real estate market is flat on its back and being dragged down particularly in the condo markets. What's worst is the continuous falling rent, mainly driven by lower immigration and weaker economy, causing one of the highest condo inventory recorded both in Toronto and in the Fraser Valley area (i.e Surrey, Langley). There will be further downward price pressure on rent, and so will condo prices in the aforementioned areas.

2. The Vancouver real estate had the second worst month of sales in March, with monthly sales dipping further to -36.8% (compared to -28.9% in February) below the 10 year average, while total inventory is up +44.9% (compared to +36.4 in February) above the 10 year average. The spread between the sales and inventory in Feb/March was 65.3% (Feb) and 81.7% (March). Anyone who says they can make a prediction now is as good as flipping a coin. Benchmark price edged up slightly by +0.5% compared to February, but do keep in mind that price is a lagging indicator, so a drop in sales now will most likely be reflected in 2-3 months down the road.

3. In a surprising move to some experts, the Bank of Canada held it's rate at 2.75% in the face of extreme uncertainty. Like most investors who opt to hold their positions now, the Bank of Canada is to stay put is a debatable yet logical decision, which I believe mainly is to keep inflation in check around 2%. If the Canadian economy worsened quickly in the summer and the inflation runs rampant due to tariffs, then Bank of Canada would be quickly under fire (again). I'm sure Tiff Macklem (governor of Canada) knows a thing or two about that.

4. If there's one thing certain about the real estate market now, that would be investors have completely disappeared. Of the many people that I spoke with, there were no investor overjoyed in the real estate discussion. As the pre-sale market nearly grinds to a halt, so has the investor confidence in the futures market. Vancouver real estate, which was once considered the safe haven and was bullet proof to global recession, may now face a prolonged period of stagnant growth, or possibly the lost decade that happened in 1993-2002. Well, on the bright side, Vancouver is still faring better than Toronto.

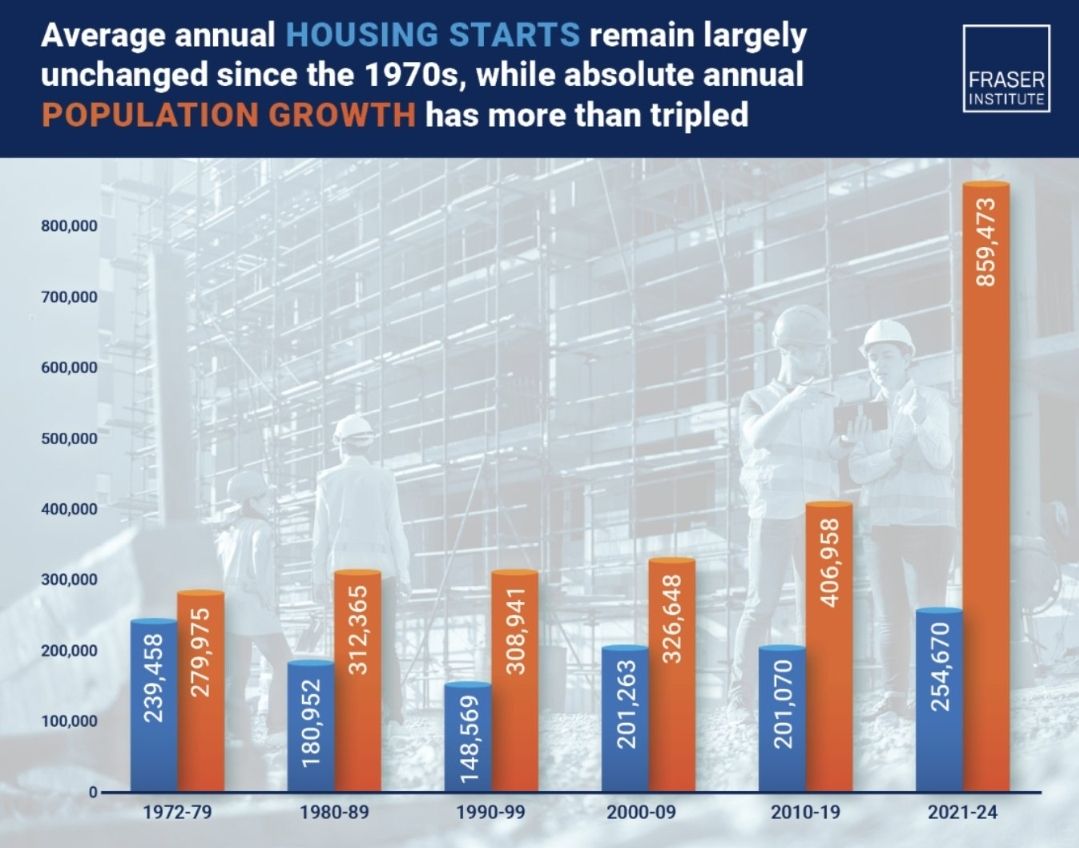

5. With the Canada federal election coming up, each party's housing policy will be a hot topic. With housing affordability remaining out of reach for many Canadians, the Conservatives are cutting red tape, reducing building permit times drastically and selling 15% of the 37,000 government buildings and turning them into affordable housing. As for the Liberals, they propose an ambitious plan of building 500,000 homes a year. To put that into perspective, the most homes Canada has ever built recently were 254,670 unit per year between 2021-2024. So to double that would either be impossible or would be just be an outright lie. Also, the homes being built would be rental housing. In other words, let's have Canadians rent happily ever after and never own their homes?

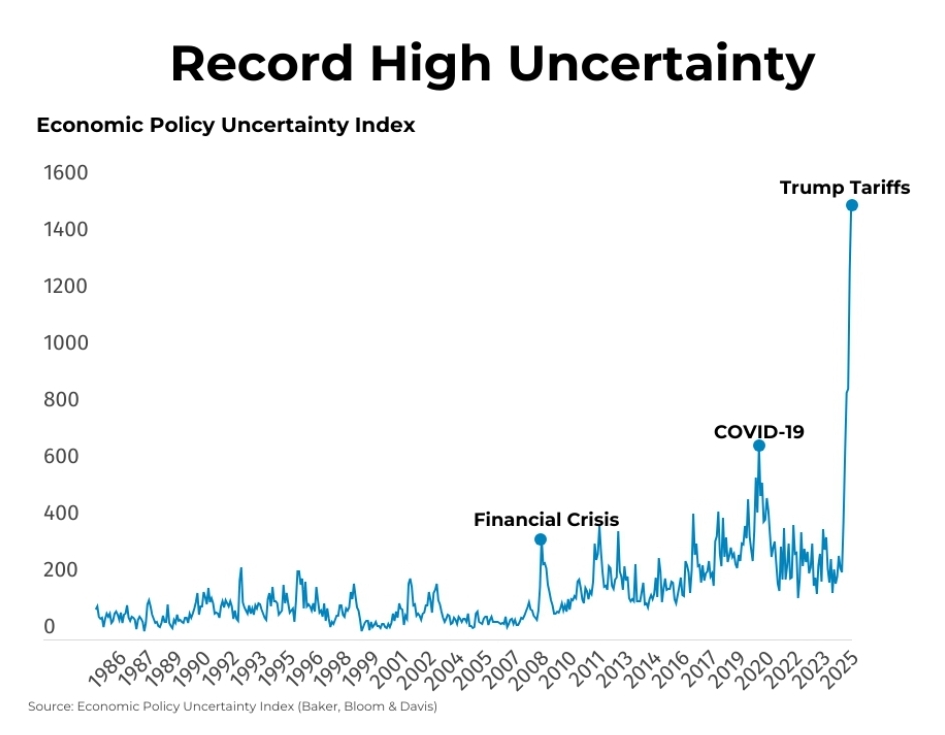

6. To say April has been a historic volatile month was an understatement. The US stock market dropped -13.7% from April 2-8, before recovering for the single best day for +9.5% on April 9. Some say that the stock market is manipulated. The volatility index has touched points not seen since the Global Financial Crisis, and is in fact 2.5x higher than that of the pandemic shutdown. As the trade war continues and a global recession looms, Canadians may find comfortable in staying liquid and not making any major investments decisions. That means real estate market will most likely remain stagnant until either the dust settles, or when we can used to the volatility.

Here are the 3 highlights for March:

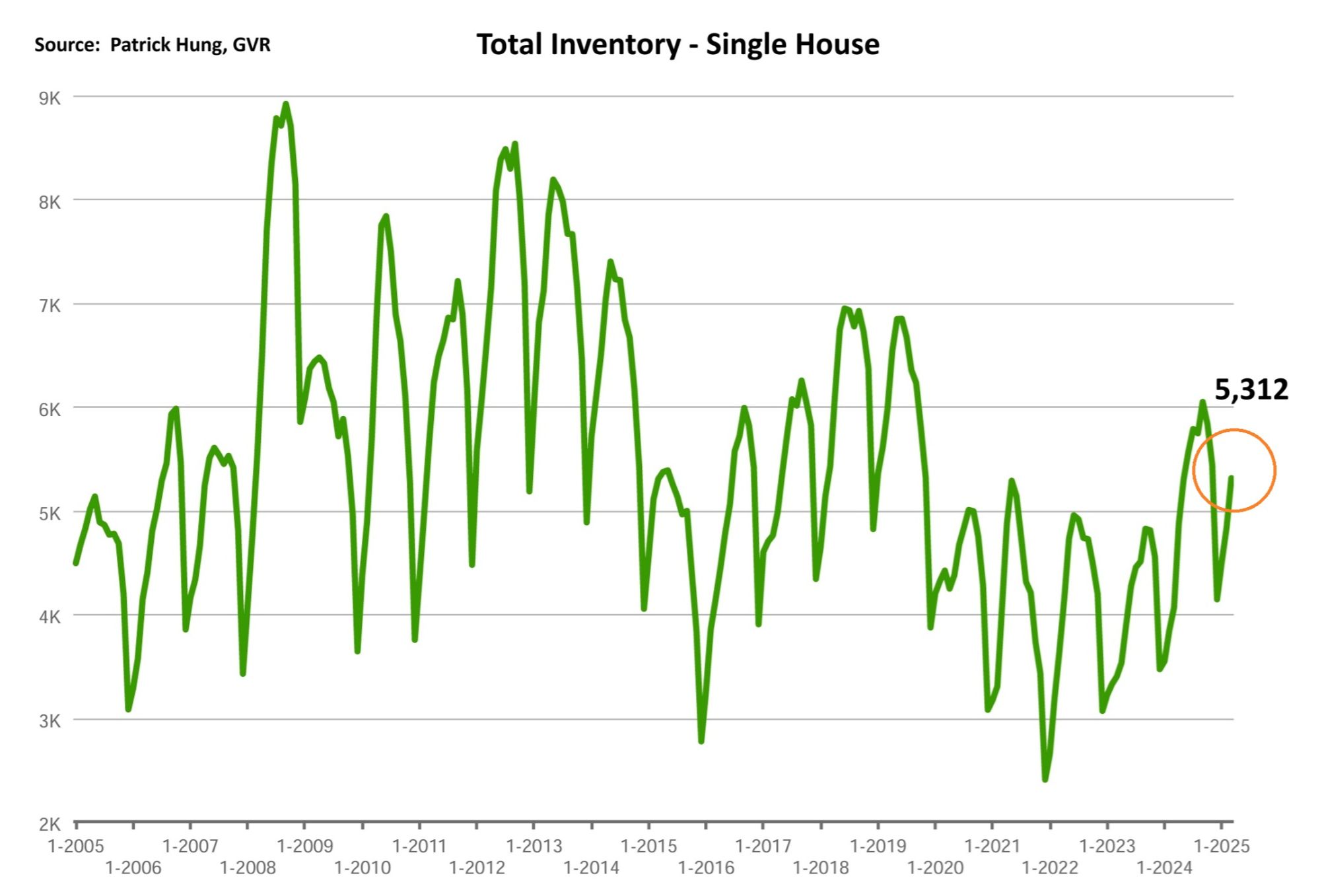

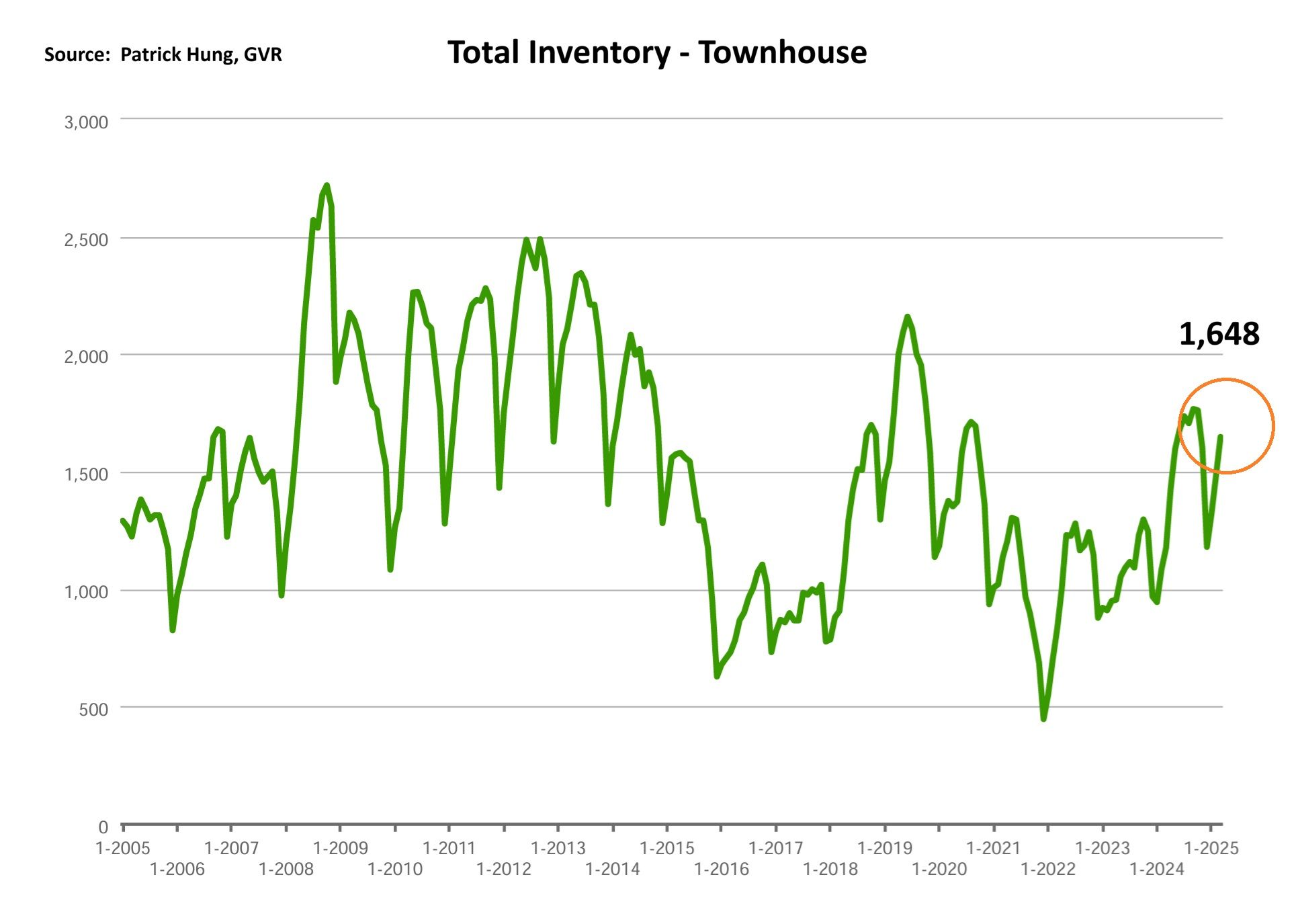

- Total inventory of 14,159 units is the highest March total inventory since March 2014.

- March was supposedly to be one of the busiest months for real estate, but it turned out to be much cooler than expected. Spring has sprung, flowers have bloomed, but the Vancouver real estate market is cold and sluggish.

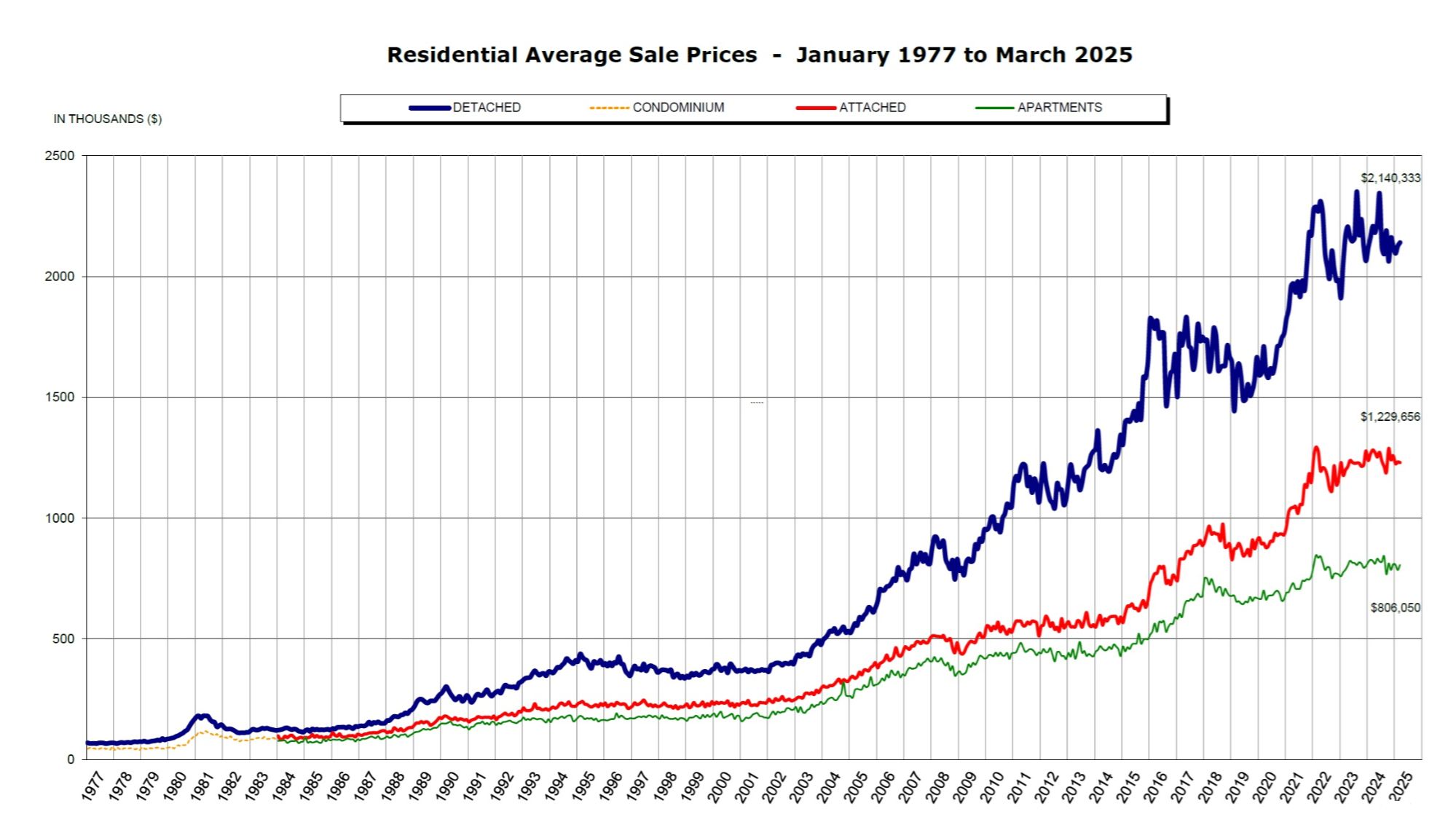

- Prices edged up slightly last month by +0.5%, and for the past 3 months the average price only edged up slightly at +1.7% since January.

Here are the in-depth statistics of the March:

- Last month's sales were -36.8% below the 10 year March's sales average.

- Month by month residential home sales increased by +13.2% from February 2025.

- Month by month new home listings has spiked by +21.4% compared to February 2025. We are reaching one of the highest inventory market since 2019, especially in the condo segment.

- Last month's price remain nearly flat at +0.5%.

- Sales-to-listing (or % of homes sold) ratio is remained flat at 14.9% (compared 14.8% in February). By property type, the ratio is 10.3% for single houses, 21.5% for townhouses, and 16.2% for apartments/condos.

Download March 2025 Vancouver Real Estate Report

Single House Market

On the surface, the single house market looks nearly identical in March as in February. On the month to month basis, sales ratio (% of homes sold) difference was only off by +0.1%, price was nearly flat as well at +0.4%, and month-over-month total inventory increase of 9% was in line with seasonality changes. However, the overall market sentiment is shifting, and signs of cracks are showing. Single house, which was one of the most solid and bullet-proof segment, are starting to see asking prices come down. As the single house remains in a Buyers market for the third straight month, downward price pressure is creeping in. Sellers who were once firm on their prices are now seeing their home sit on the market for 60 or 90 days. Meanwhile, more competitors are coming onboard. What's worst is that even when homes are sharply priced, they still take longer than usual to sell. Some agents shuffle their strategies (i.e lower list price generating multiple offers) but still failed to materialize: either there are no offers, or offer prices were too low. As such, the entry level price range is starting to shift slightly downward as well. What was once a rare scene of seeing homes sold for $1.5m - $1.6m are popping up again in Vancouver East, Burnaby, and Richmond. Overall, single house Buyers remain fearful of overpaying and seem to have no problem waiting in hopes of more clarity from the trade war. As such, it is nearly impossible to know what tomorrow holds, but it does look like there will be more downward price pressure, at least in the next few months for the single house.

For the month of March, the neighorhoods that registered most price growth were Pitt Meadows, Whistler and Squamish, posting +4.4%, +3.7% and +3.4% respectively. Conversely, the neighborhoods registered the most significant price drops were Bowen Island, Sunshine Coast, and Coquitlam, with -2.4%, -1.4% and -0.6% respectively. The single house market has remained in a Buyers market for the past 3 months, with average days on market dropping significantly to 35 days (compared to 45 days in February), and month-to-month average price went up slightly to +0.4%. Sales-to-listing ratio (% of homes sold) remain nearly unchanged at 10.3%. (compared to 10.7% in February).

Apartment and Condo Market Since the beginning of the year, the apartment market has been flooded with new supply, and last month was no different. In fact, March was the highest supplied month of apartments in Fraser Valley, and Vancouver's was the second highest for the month on record (2012 took the crown). As the months go on, inventory continue to pile up, causing the greatest downward price pressure in a decade. What's worst is that in the upcoming months, there are even more new apartments about to be completed, meaning there will be more fresh supply to compete with re-sales. Even though last month the apartment market seemed to have the best performance with the highest price growth (+1%) in all segments, but deep down I believe that is merely a smoke screen as we are likely to face steeper price drops in the upcoming months. As immigration slows and rental rates continue to fall, more and more apartment investors have decided to flee the scene and put their investment home on the market. However, we are now at a crossroads where such Sellers are slow to react, such as the case when they have placed their homes on the market for 90 days but is getting no bite, no offer and very little showing request. In other words, apartment Sellers are having a hard time adjusting to the downward trending market. Indeed, it is a hard pill to swallow, since Greater Vancouver apartments has had a long history of investment glory. When this trend started to shift last year, some Sellers reacted quickly, and it was those that came out on top. It may be months or even years before apartment Seller can accept the current market, but by then, tenths and thousands of dollars would've been lost on the hopes and dreams of the past. My advice to the apartment Sellers now is to quick to come to the their senses. The sooner they accept the current market, the more they are able to cut their losses. In an over-supplied, downward trending market such as the apartment is now, an offer price now is most likely better than the one a month or two later. For the month of March, the best performing neighbourhoods for apartments are Richmond, Ladner and Vancouver East, at +1.9% (tied for 1st) and +1.7% respectively. Conversely, the areas with the most significant price drops were all in the outskirts in Sunshine Coast, Pitt Meadows and Maple Ridge, posting -1%, -0.8% and -0.6% respectively. The apartment and condo segment remained in a balanced market for the fourth straight month, with average days dropping to 28 days (compared to 37 days in February). Month-to-month sale price went up slightly by +1% (compared to -0.1% in February). Sale-to-listing (% homes sold) ratio also remained nearly flat at 16.2% (compared to 16.8% in February).

Here are the Three Trends I'm Observing:

2. Double?

|

Recent Posts

GET MORE INFORMATION