Real Estate Market Intelligence May 2025

Real Estate Market Intelligence May 2025

|

Download April 2025 Vancouver Real Estate Market Report

Single House Market

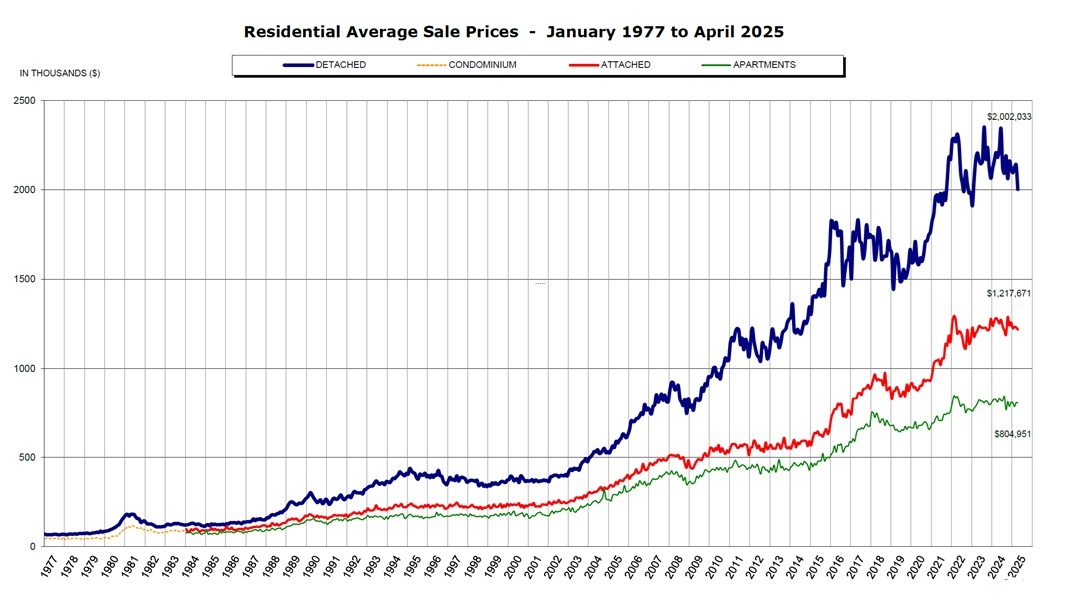

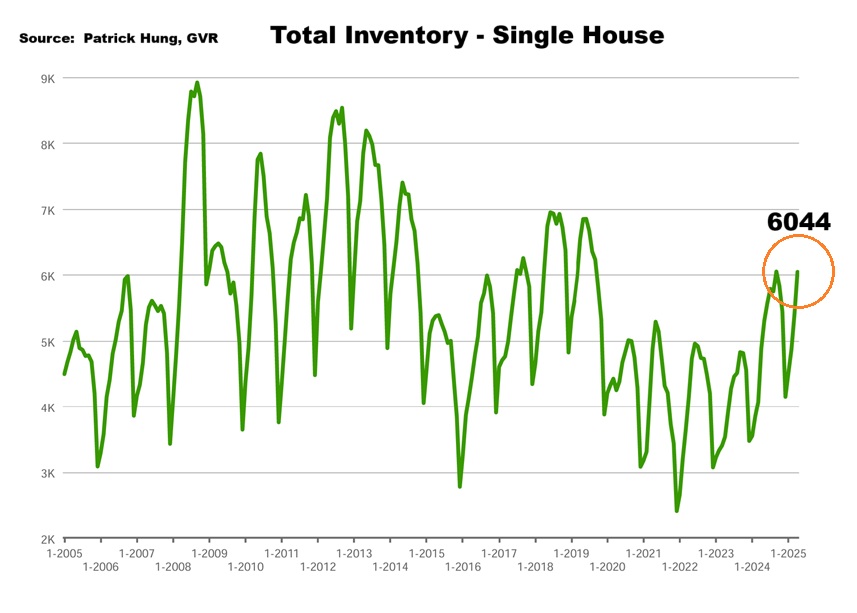

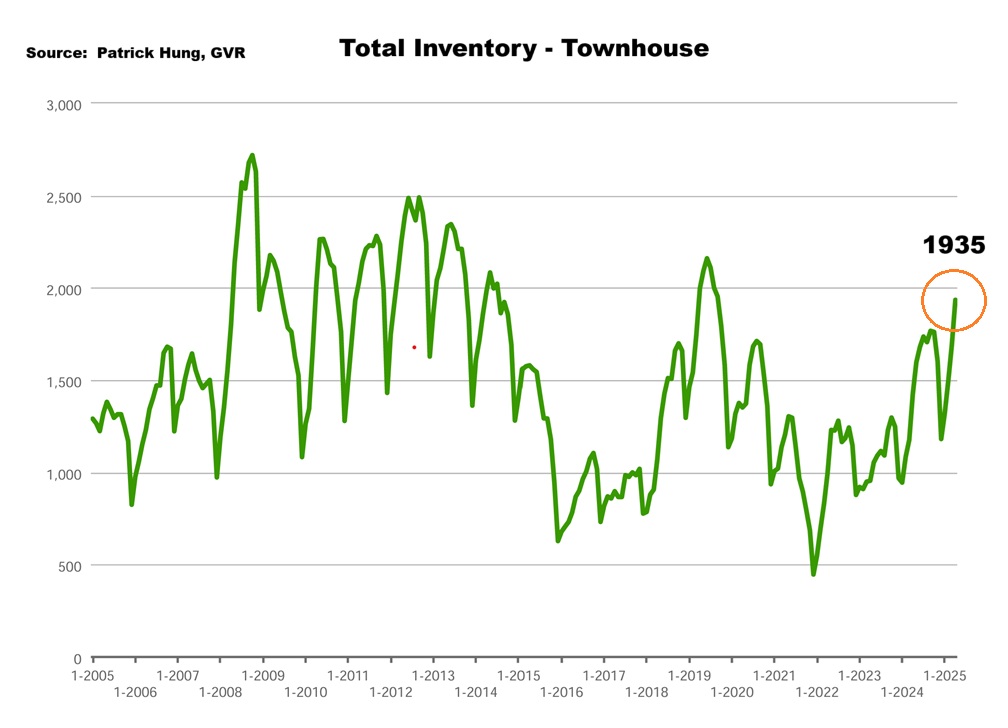

The cracks in the single house market is becoming more evident in April. Overall single house house supply went up by +10.6% month-over-month as more Sellers come off the sidelines. It was as though the market has hit a capitulation point, and after months of hanging onto the ghosts of the past where single houses were resilient and firm, they have finally come to their senses. Key is, as we start to see the sold price come down in the past few months, Sellers asking price now are also coming down. This tells me the Sellers are aware of further negative price pressure up ahead, and is adjusting their selling position. Having said that, demand is still weak with sales-to-listing ratio (% of homes sold) dipping to a single digit to 9.9%. This definitely come as a surprise as April and May were supposedly to be the busiest time for real estate of the year, and yet single house Buyers continue to hold off. Based on the conversations I've had with other top producers in the industry, we have seen single house traffic at open house and private showings being choppy, with on-again off-again weeks. In some neighborhoods, we are seeing another intriguing trend emerging: what was once considered a bottom line for entry level priced homes (i.e $1.6m in East Vancouver or Richmond) has now been breached. This definitely was a welcoming sign for single house Buyers, but it remains to be seen just how long this breached bottom price line stays in place. On the other hand, luxury market also took a beating this year, with home over $4m having Q1 sales dipping 48% year-over-year. As we continue to see more inventory flood the market, it's really hard to see how any price recovery could be in sight in the summer.

For the month of April, the neighorhoods that registered most price growth were Whistler, West Vancouver and Maple Ridge, posting +2.7%, +2.1% and +1.3% respectively. Conversely, the neighborhoods registered the most significant price drops were Bowen Island, Sunshine Coast, and Port Moody, with -3.8% (tied for 1st) and -2.4% respectively. The single house market continues to be in a Buyers market for the past 4 months, with average days on market remaining at 35 days (same as March), and month-to-month average price dropped slightly to -0.6%. Sales-to-listing ratio (% of homes sold) remain dropped further and is now at a single digit at 9.9%. (compared to 10.3% in March).

|

Apartment and Condo Market

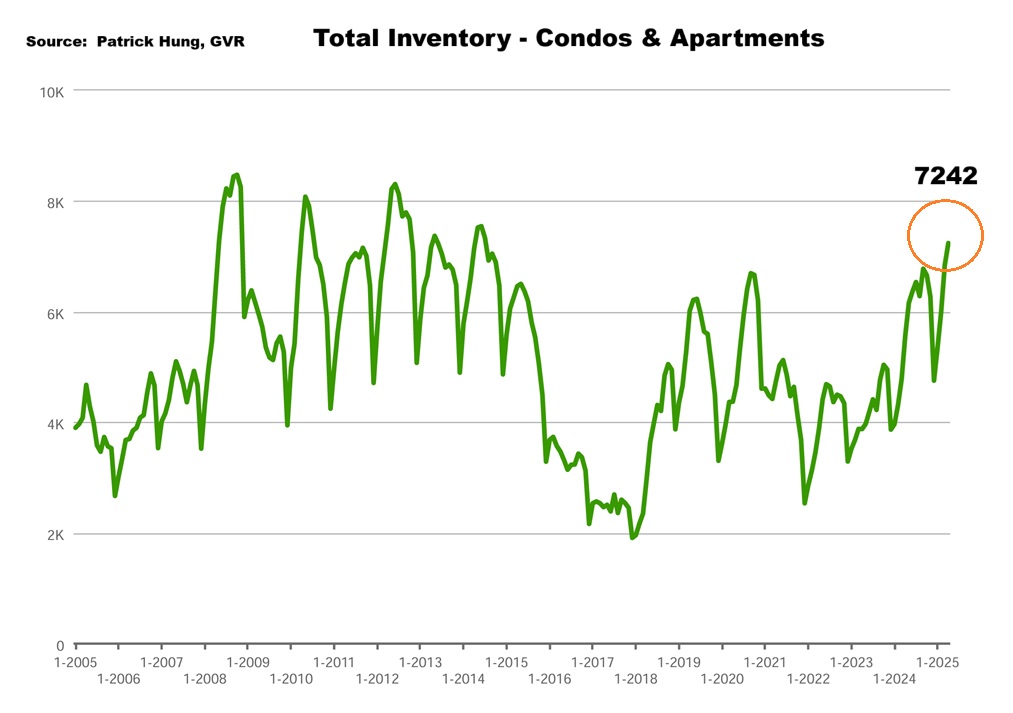

In short, the current decade-high supply in Vancouver real estate inventory was mainly driven by the surge in condo listings. As previously mentioned, there were simply too much construction that's completing this year (and next year), and they are all competing in the same space with the re-sale. Add the mom-and-pop condo investors who are liquidating due to the falling rent, and it's not hard to see why this segment is skewing the market. Month-by-month listings continue to climb higher by +5.5%, while sales stayed nearly on par with +4.3% gains within the same period. Surely, neighborhood trends are still polarizing, with Vancouver downtown core's condo inventory at 9 months (4 months is healthy). With boots on the ground, it certainly feels like the condo market is in much deeper water than the stats show, especially for the pre-sale construction. Having said that, more bad news of coming out of that pre-sale space as one developer's project, who has just tried selling for a few months but is getting very little interest, has decided to call it quits and return all deposits to the Buyers. Another news on one of Vancouver's biggest pre-sale marketing company, Rennie, has just laid off 25% of their workforce due to more challenging concerns. There is simply no where to run nor hide in this condo space. When the prices that were sold 2-3 years ago has exceed the value it is now, just who is going to buy that? In Toronto, nightmare stories are getting more common as class lawsuits were launched against Buyers who cannot complete their pre-sale purchase. For example, if they had bought a pre-sale 2 years ago for $1m, and now the current market value is at $780k, their 20% deposit of $200k has evaporate, PLUS buyers are now on the hook for more money to complete as the banks will not loan at original purchase price of $1m, but at market value $780k. When investors were overstretching and are now deep in water, their negative equity will have long-lasting effects on the market. I just cannot imagine how this segment will improve this nor next year, and fully expect further downward price pressure to continue, and may even pick up pace.

For the month of April, the best performing neighbourhoods for apartments were all in the outskirts of Squamish, Sunshine Coast and Whistler at +2.8%, +2.7% and +1.2% respectively. Conversely, the areas with the most significant price drops were West Vancouver, Burnaby Noth and Richmond, posting -3.9%, -1.8% and -1.7% respectively. The apartment and condo segment remained in a balanced market for the fifth straight month, with average days increasing slight to 31 days (compared to 28 days in March). Month-to-month sale price dropped slightly by -0.6% (compared to +1% in March). Sale-to-listing (% homes sold) ratio also remained nearly flat at 15.7% (compared to 16.2% in March).

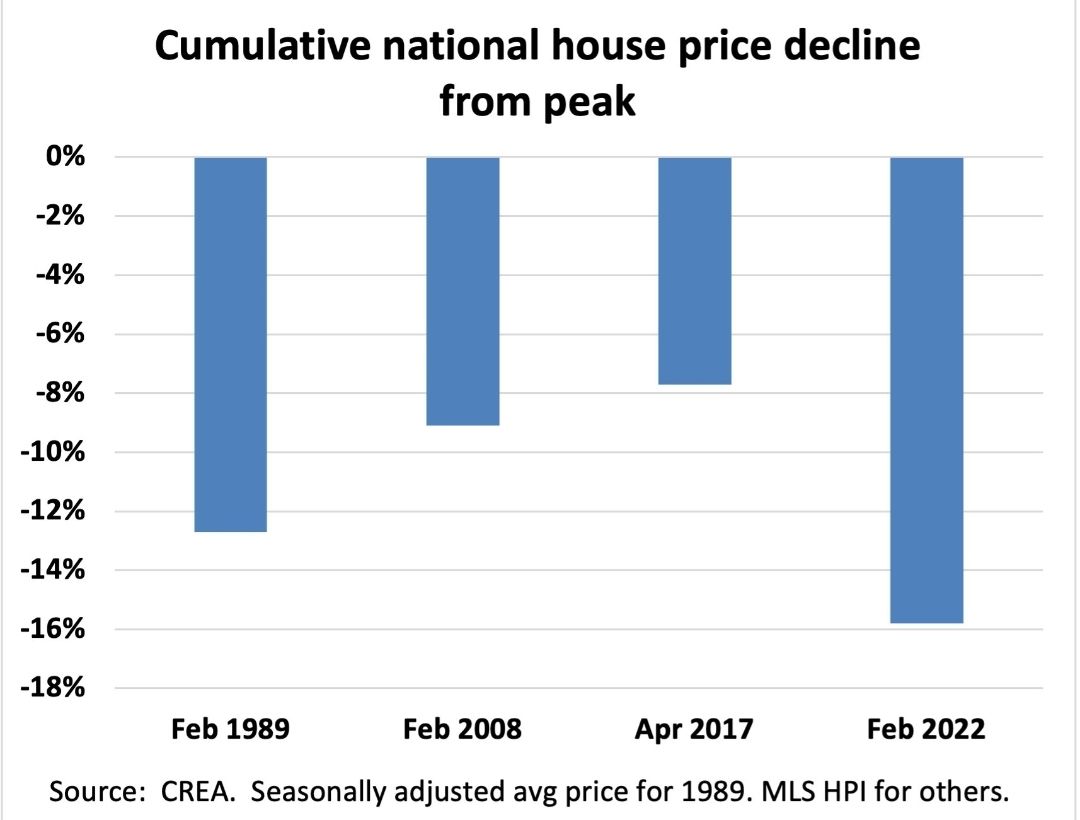

1. Correction

Home prices in Canada (mainly Toronto and Vancouver) has dipped nearly -16% from peak of Feb 2022 to present, and is the biggest housing price correction since data was recorded back in 1989. What's worst is that it remains on a downward trajectory. Unless we see some unexpected good news to come out of Canada, there will be more pain to come as we close in on -20% mark. (Source: CREA, Canadian Real Estate Association)

2. Stagflation

Canada's inflation cooled in April to 1.7% mainly due to the removal of carbon tax. However, core inflation has risen to above 3%, which is in an alarming zone. No matter how the Canadian government denies it, the rising unemployment rate compounded with rising inflation is the definition of stagflation. With this in mind, all bets are off on where the upcoming Bank of Canada rate cuts would be. It has become very likely that we will see no further rate cuts till the end of summer.

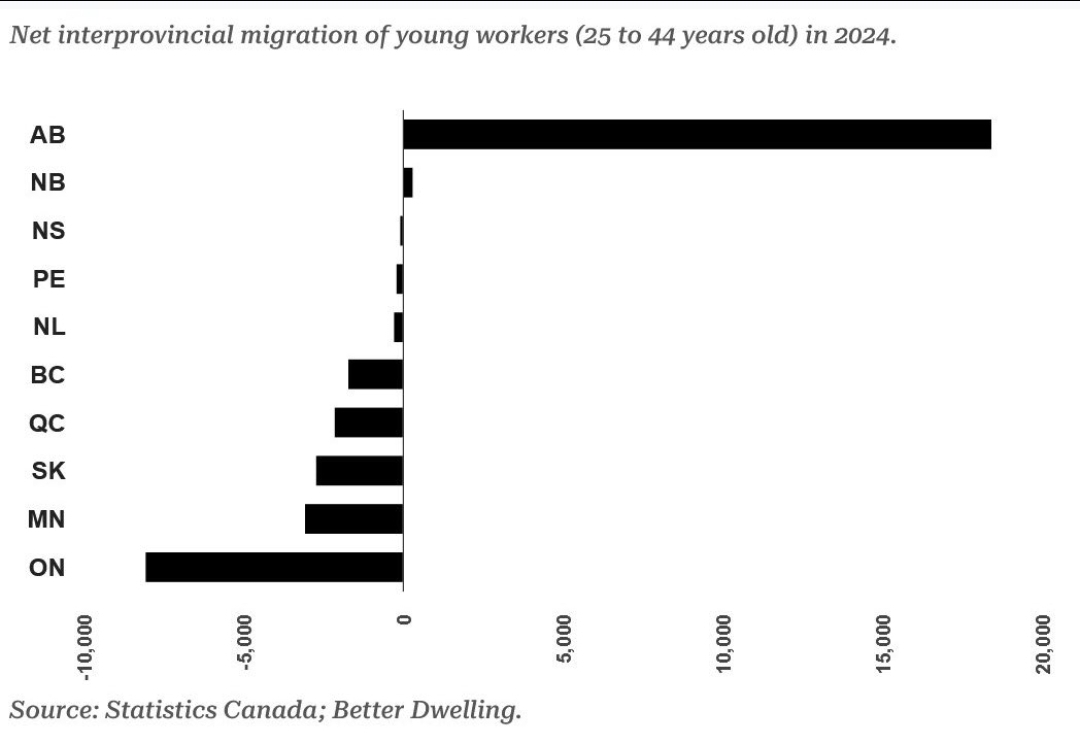

3. Alberta Keeps Calling

Even when housing prices are coming down, affordability remain a huge issue for many Canadians in Toronto and Vancouver, especially those between 25 to 44 years old. For this same reason, those in this age group continue to seek a better standard of living in Alberta. With the "newer" Liberal government not having any plans of making homes more affordable, perhaps moving to Alberta would soon not even be a viable option anymore: younger Canadians will just leave the country altogether. (Source: Statistic Canada, Better Dwelling)

Recent Posts

GET MORE INFORMATION