Real Estate Market Intelligence September 2025

As summer is nearing to an end, school has finally resumed and families are now back to the normal routines. As such, September is the month where I've emphasized all along of its importance; where real estate Buyers and Sellers make a final push before the year end and begin to set the tone for Q4. Again, the atypical trend continues this year where slower summer months were not slow (activities started to pick up in July), and busy spring season was not busy (lowest May sales in 20 years). Last month, the Vancouver real estate continue to climb out of record sluggish sales. With that said, I've seen some fellow agents and mortgage brokers preach via social media about "improving" markets. There certainly is some truth to it, with sales going from record 20 year lows, to now 10 year low (still bad in my opinion). On the demand side, August's "increased" sales still rings in -19.2% below the 10 year average. On the supply side, Sellers continue to enter the market and remained +36.9% above the 10 year average. The August spread between the two has improved to 56.1%. For context, this was at one point near 80% in May-June. The key psychological changes in August are; Sellers accepting the reality of lower prices, and Buyers accepting the risk of overpaying. I believe it all started with Sellers, who had been firm believers in the Vancouver bullish market and thinking it will always recover, began to see their patience run thin. Some are finally starting to question: "What if this time the market will continue to drop for more months to come?" With more competition piling up (and at lower prices), it was only a matter of time before downward price pressure breaks the Sellers. And in August, we saw exactly that. Prices began to ease and Buyers began to absorb the inventory, and as sales improve, the market slowly regains its footing. It is still early to say whether this is a trend or a blip on the map, but at least the sales are improving. Lots to cover again this month as the Canadian economy continues to deteriorate with unemployment rate in August climbing to 7.1%, Canada's real GDP declines by -0.5% in Q2, inflation jumped slightly to 1.9%, and more news of BC and Ontario developers folding. Also, an important Bank of Canada rate announcement tomorrow. Let's dive deeper.

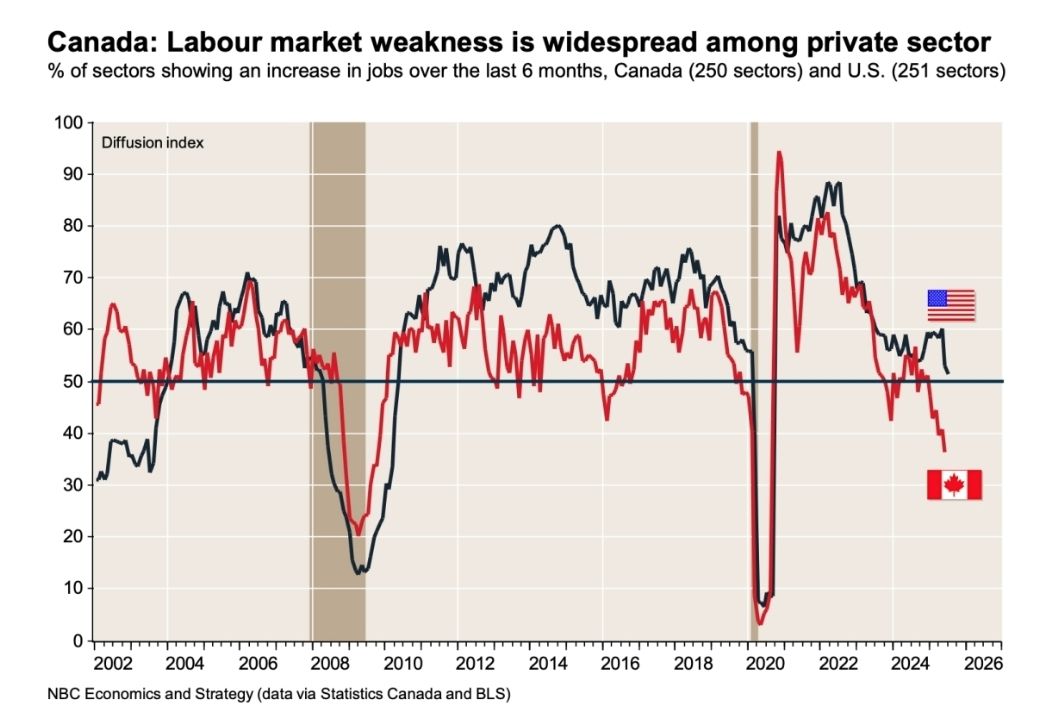

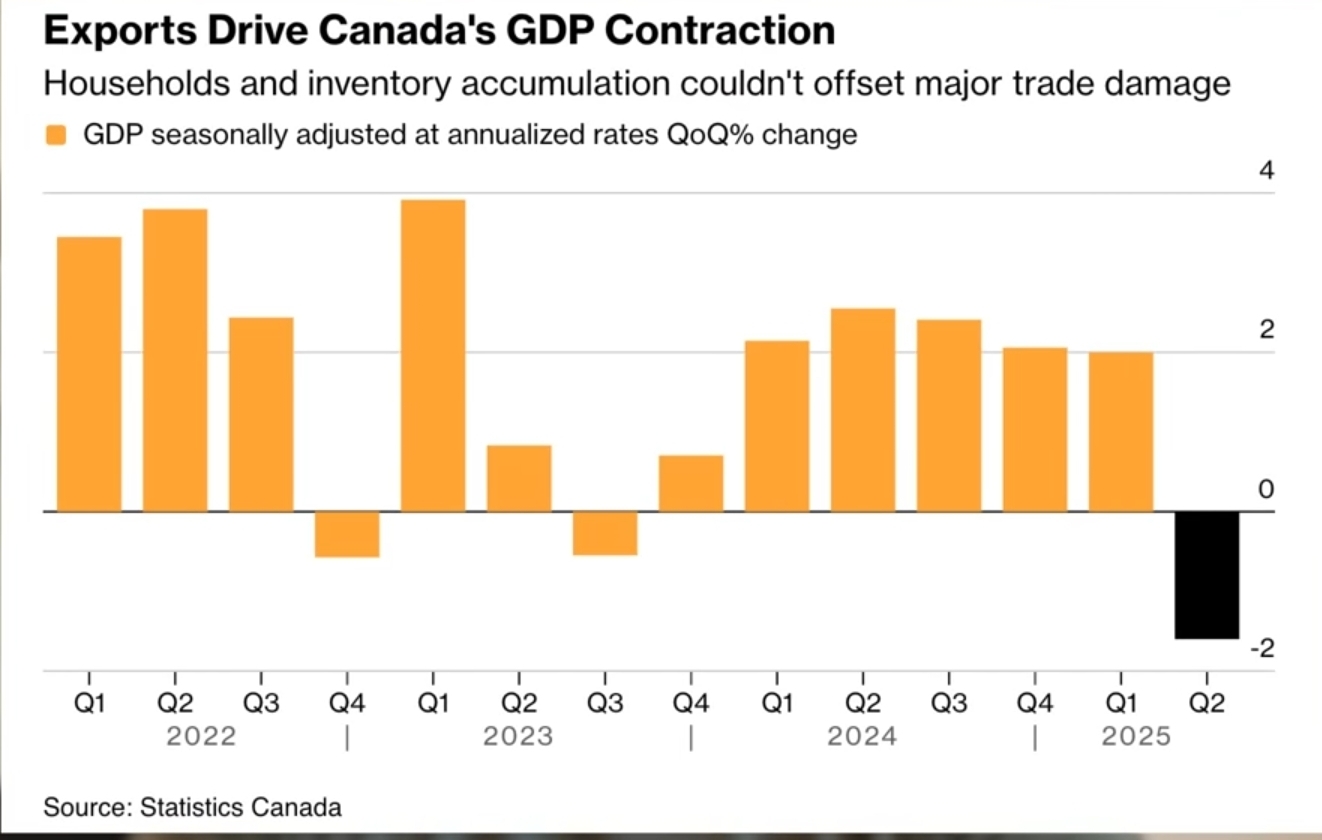

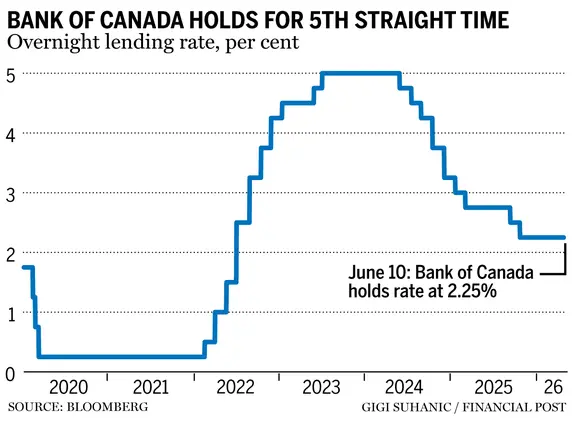

So far this year, I don't recall hearing any upbeat economic news coming out of Canada. In August, the unemployment rate jumped to 7.1%, which is the highest levels in nine years outside of the pandemic. 60,000 jobs slashed were slashed, and combine that with July's 41,000 job loss, we have over 100,000 jobs vanished in two months. Cities in Ontario such Windsor was hit with a agonizing 13.1% in unemployment, and Toronto is closing to double digit at 9.9%. Vancouver is sitting near the national average at 7.2%. With more steel, aluminum and auto workers getting laid off on Ontario, it's not difficult to imagine why the real estate market there is crumbling faster than the rest of the country. Moreover, Canada's GDP tanks at -1.6% annualized, and again the biggest decline since the pandemic. A report from National Bank says only 36% of private sector industries have grown on the past six months, and this is unheard of outside of a recession. All these bad news rained down on Bank of Canada as the market odds of a rate cut surges to 80% in the upcoming announcement tomorrow. And even with lower interest rates, there is no stopping developers in BC and Ontario from folding their projects. Wesgroup, one of the the largest developers in Vancouver, has just cancelled a project that was 60% sold with deposits were returned to Buyers. Also, the owner of the now defunct Thind Properties, Daljit Thind, had his own home sold under receivership for $13.6m. More bodies are floating to the surface as the construction industry contracts.

Moving forward, the volatility continues as the first two weeks of September saw further increase in traffic in Vancouver real estate. More Buyers are shopping but it awaits to be seen whether they translate into offers and sales. Another trend I've observed is that more Sellers are now trying to get ahead of the market by lowering listing price and doing multiple offer bidding. The Sellers' urgency to move their products before end of the year is clear, but the market is still in a state of elevated inventory (10 year high for August) where Buyer has tons of options. Thus, most Buyers are not in the mood the bid, and even if they do, it would be with a clear conscious. Good products still move fast, regardless of the market, but its the medium to bad products that's dragging down the entire market and applying further price pressure. As the winds continue to change quickly, there is only a 6-8 week window now before the winter seasonal cool down. Seller either try to push hard now, or will have to wait till February-March of next year to reboot. As for Buyers, there are plenty of great deals to be had, and enjoy the good times as this was really a once a decade phenomenon in Vancouver real estate. In my opinion, some segments will hit a price floor sooner than others, and apartments, especially those in investor-heavy areas such as Guildford (Surrey), Brentwood (Burnaby), and River District (Vancouver) will continue to face stronger headwinds in downward price pressure. With the Bank of Canada's rate cut announcement tomorrow that's highly anticipated to be -0.25, it won't move the needle, but may just be enough to get some Buyers to come off the sidelines. Let's see.

Some of the unique trends I've been observing:

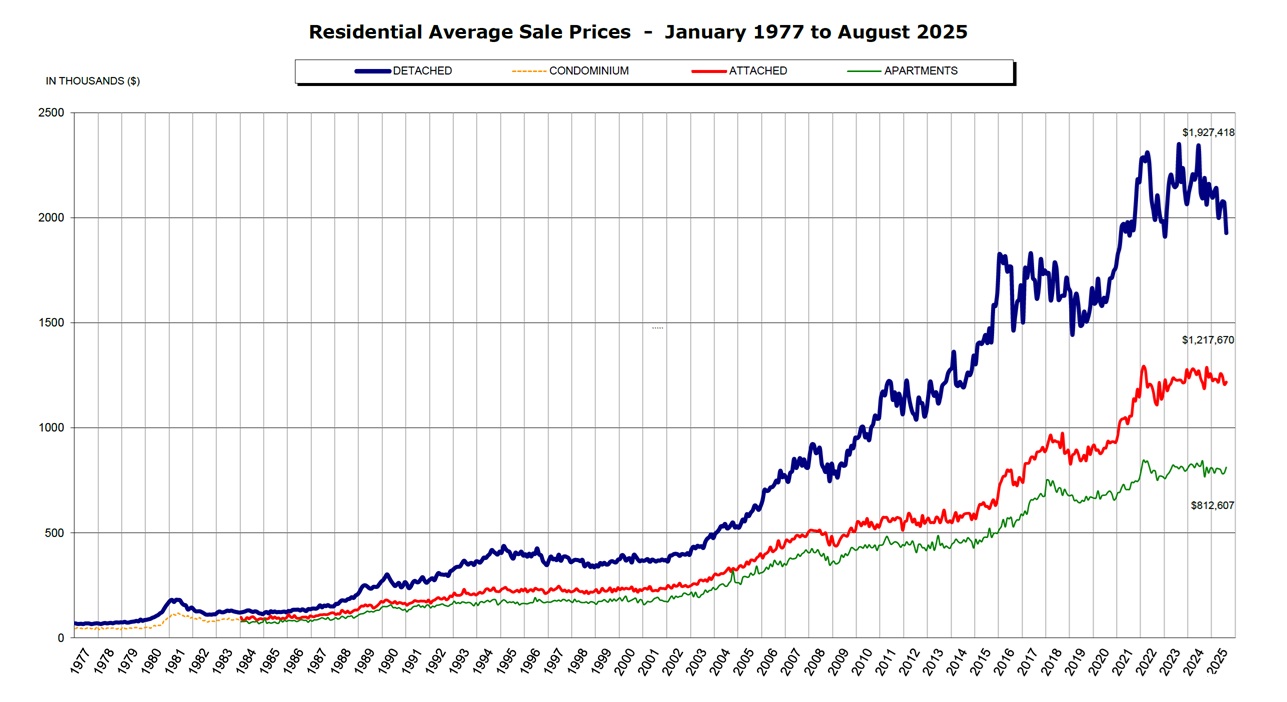

1. The Vancouver real estate market in August maintained its momentum from July, but did see some seasonal effects kicking in. Surprisingly, year-over-year August sales shot up slightly by +2.8% compared to 2024. However, diving deeper and we see sales are still weak, with sales -19.2% below the 10 year average and total inventory at +36.9% above 10 year average. The psyche has changed and Sellers are now accepted the reality of lower prices, and buyers (although getting more picky with a wide range of selection) are starting to come off the sidelines. There is improvement going from 20-year low in sales to 10 year low, but again anything coming off an ice-cold market may be considered warm. I still think there's ways to go.

2. Canada's latest unemployment came in at 7.1% (up from 6.9% in July) and saw 60,000 jobs slashed. With July and August combined, there were over 100,000 jobs lost in two months. That's massive and the lagging indicator is finally showing the Canadian economy is not as resilient as it is claimed to be. Again, the mass import of 3 million immigrants (such temporarily workers) over the past 3 years exasperate the problem multi-fold. Don't expect the federal government to relax immigration anytime soon.

3. Calgary's year-over-year rent dropped 10% and bounds to keep falling with record supply down the pipeline. This is the joy of the free market, where municipalities have very little red tape over building and rent control.

4. If the silent resignation is a new norm, then developers in BC and Ontario are jumping on board. What has not been advertised are projects, such as one called Ardea in the River District, is being cancelled. Its developer, Wesgroup, is one of Vancouver's prominent developer. What was interesting is that 60% of this building is sold, which means it can secure financing if needed. But the fact that Wesgroup still decided to cut it loose means there is no more glaring evidence than that the pre-sale market is bellies up. Beware: more bodies will float to the surface soon.

5. When talking about Canadian real estate, one usually refers to two of the biggest markets: Toronto and Vancouver. As we know these two markets are hurting now, what about other provinces? Interestingly, they are performing quite well. For example, Newfoundland, Quebec and Saskatchewan all registered year-over-year growth of +11%, +9.5% and +8.1% respectively. While the most populous Canadian cities are getting scarred, other smaller cities seem to be doing just fine.

Here are the 3 highlights for August:

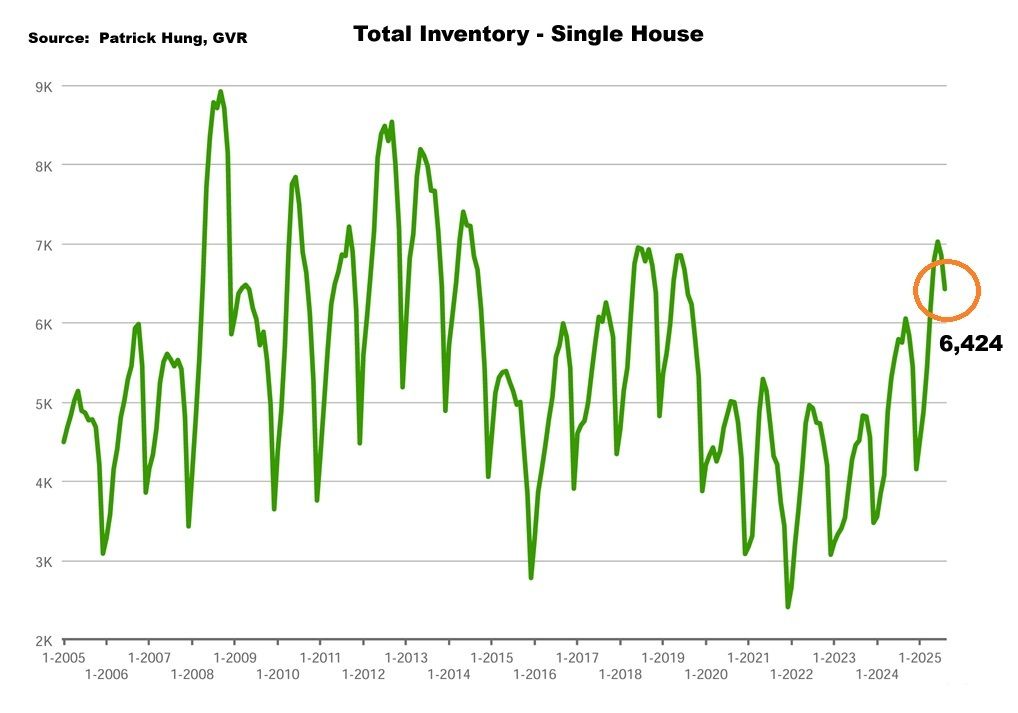

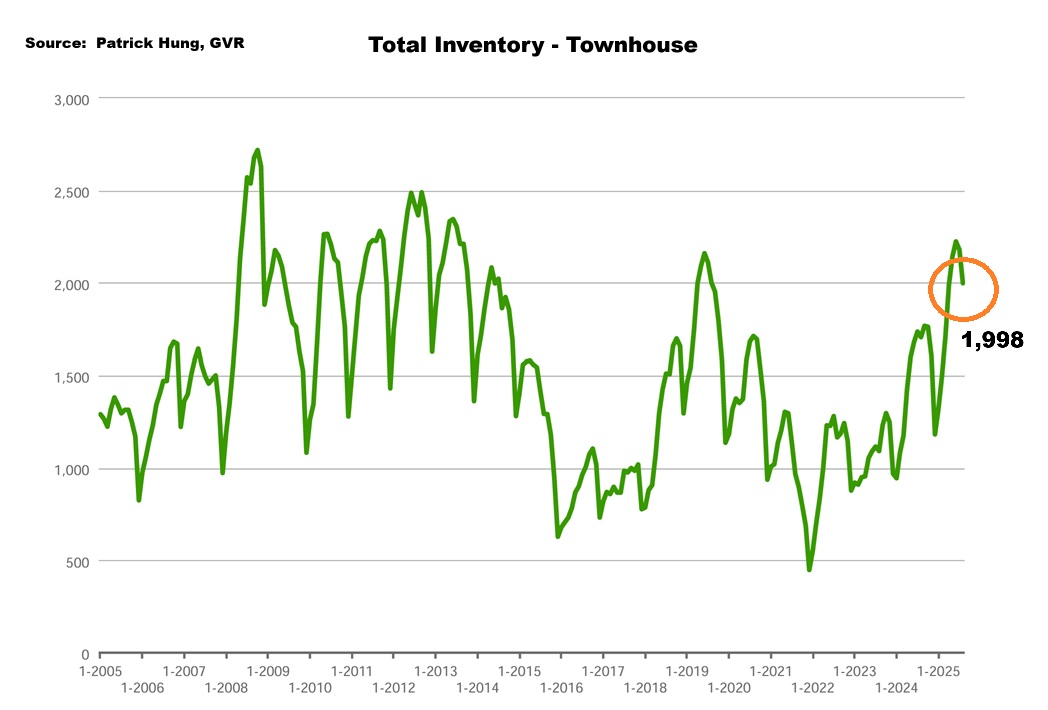

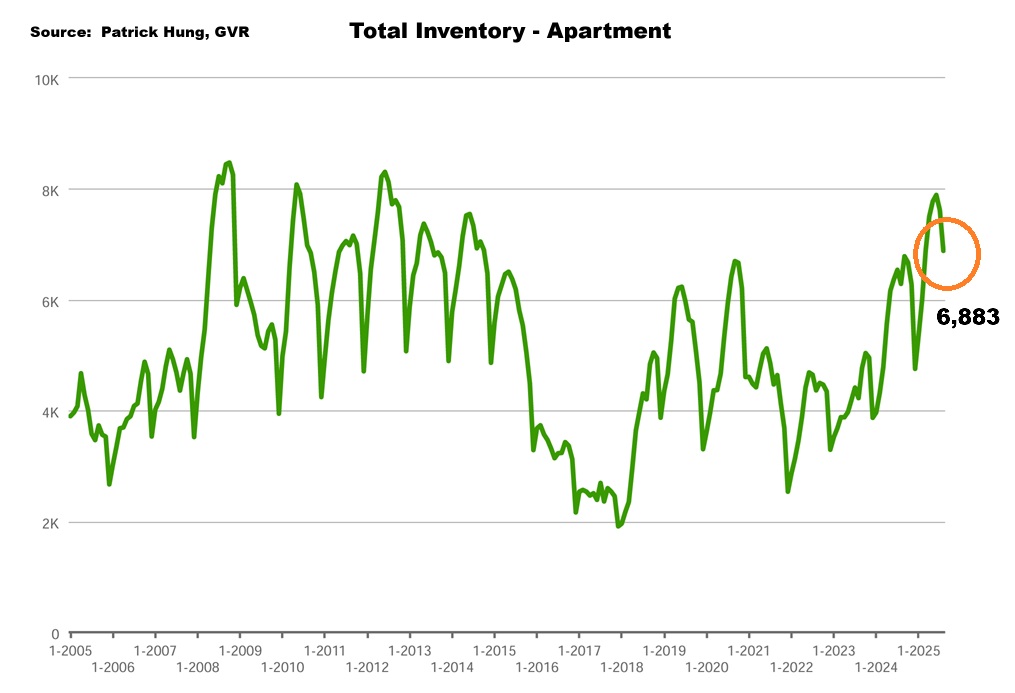

- Total inventory of 16,242 units is the highest August total inventory since 2013. Even though there are more sales to balance the market, Sellers continue to enter the market faster than Buyers can digest.

- The first two weeks saw increased activities in August, but fizzled in last week with more local families go on end of summer vacation.

- Prices continue to slip and is picking up pace, with average prices month-to-month dropped by -1.3%, and by a total of -2.3% in the past 3 months. The 3-month price drop came from apartment (-3%), townhouse (-2.5%) and single houses (-2.3%).

Here are the in-depth statistics of the August:

- Last month's sales were -19.2% below the 10 year July's sales average. (compared to -13.9% in July)

- Month by month residential home sales dropped sharply by -17.5% from July 2025, partially due to seasonality.

- Month by month new home listings dropped sharply by -33.8% compared to July 2025. Some Sellers are electing to relist at a new price in September to make that final push before year end.

- Last month's price dropped further by -1.3% (compared to -0.7% in July)

- Sales-to-listing (or % of homes sold) ratio is increased slightly to 12.4% (compared 13.8% in July). By property type, the ratio is 9.3% for single houses, 15.8% for townhouses, and 14% for condos.

Download August 2025 Greater Vancouver Real Estate Report

Single House Market

In August, the single house market seem to be stuck in a funk, with steady traffic but still a low sale-to-listing ratio (% of homes sold) at single digit 9.3%, which is the lowest across all segments. Again, more window shoppers but no bite. Month-to-month sales has dropped -14.6%, which is in line with seasonality. Key is, monthly total inventory slipped at -6.9%. On paper, demand is dropping faster than supply. Keep in mind that September is typically the month where a wave of Sellers come onto the market to make that final push of the year, so expect the single house market to be flooded with even more inventory and motivated Sellers. Anecdotally, areas such as Ladner and West Vancouver saw much steeper discounts in sold prices. Open house traffic in these areas were sparse, and competition is fierce. Thus, further downward price pressure is expected in these neighborhoods. Having said that, polarity remains as some homes in Richmond and Burnaby seem to be picking up some steam. For example, two of my single house listings in Richmond, both of which were reasonably priced and in great showing condition, attracted over 20+ groups in each weekend of the open houses and were both subsequently sold in less than 2 weeks. This is a reminder that the Buyers have NOT left the market, but are either lurking and becoming more picky, or are just tied to sale of their home first (i.e subject to sale). Good products that are sharply priced are still moving quickly, and at times I was surprised to have seen bidding with cash offers (yes that's right). Again, this does not apply to all areas as real estate is hyper local, but the key ingredients of competitive pricing combined with immaculate condition home remains the driving factors to get it sold. Last month, areas such as Richmond and Burnaby rebounded faster (and may possibly hit a price floor sooner), whereas Ladner and West Vancouver slipped further. In any case, it is one of the best times, in a decade, to be a single house Buyer now. Last month, Sellers have finally accepted the reality of price drops, with a high probability of further downward price pressure ahead, and Buyers seem to have waited long enough that they feel the price is right. Could this be a sign of a bottom? In my opinion, not yet, but the price reductions may get smaller, especially with more rate cuts in the backdrop.

For the month of August, the neighorhoods that registered most price growth Burnaby East, Bowen Island, and New Westminster, posting +1.9%, +1.8% and +0.8% respectively. Conversely, the neighborhoods registered the most significant price drops were Burnaby North, West Vancouver, and Ladner, with -3.1%, -2.8% and -2.5% respectively. The single house market continues to be in a Buyers market for the eighth consecutive month, with average days on market increasing to 47 days (compared to 42days in July), and month-to-month average price dropped by -1.2% (compared to -0.7% in July). Sales-to-listing ratio (% of homes sold) dropped back to a single digit at 9.3% (compared to 10.2% in July).

The townhouse market have taken the biggest price hit across all segments in August, with month-to-month price change at -1.8% (compared to -0.4% in July). Just as things looked to stabilize for townhouses, it got turned upside down again. Even though the sales-to-listing ratio (% of homes sold) is 15.8%, which is the best among all segments, we are seeing conflicting data with month-to-month sales dropped by a whooping -21.3% in August. Similar to the single house market, the townhouse new supply has simply outpaced that of demand. Sellers continue to left behind in adjusting to new norms, which have less open house traffic and next to no offers. For the first two weeks of September, the townhouse traffic has slowed significantly. Again, in some cases, there were Sellers and agents choosing to run ahead of others by lowering their prices to attract multiple offers. While some Sellers are genuinely and urgently need to sell, others are just testing the market. This malpractice further confused the market and thrown Buyers off-guard. For example, two similar sized townhouses within a half block away can have $250,000 difference in listing price. If the lower priced Seller's intentions are real, then such cut-throat pricing happens when only when fear overtakes them. Key is, Buyers may take it as a new norm. Anecdotally, I feel townhouses under $1m in suburbs such as Burnaby, Ladner, Richmond, and Delta still have an active market, but anything over $1.2m seem to be stuck, so the bottom-up trend continues. It looks like townhouse market is in the monthly seesaw mode and will take longer to stabilize. Perhaps the shakey apartment market would have more drag than ever on this townhouse segment.

In August, the areas with the most townhouse price growths were in Pitt Meadows, Ladner, and Tsawwasen, registering +1.6%, +1%, and +0.5% respectively. Conversely, the neighborhoods with the most significant price drops were Vancouver East, Whistler and Richmond, at -3.6%, -3.5% and -3.1% respectively. The townhouse market remained in a balanced market with days on market increased slightly to 36 days (compared to 30 days in July). Month-to-month sale price dropped significantly by -1.8% (compared to -0.4% in July). Sale-to-listing (% homes sold) ratio slipped slightly to 15.8% (compared to 16.7% in July).

Apartment Market

On the surface, the apartment market's monthly price change seems to be on par with the single house market, both seeing a drop -1.2% last month. Diving deeper, the monthly apartment sales dropped by -21.3%, which is the identical to that significant drop in townhouses. We are finally witnessing this phenomenon where plenty of new units competing in the same space as re-sale. Projects such as Hayer Town Centrein Langley, Luxe and RC at CF in Richmond are a few projects pending completion within weeks. With thousands of these new units being handed over to new homeowners, I can't help but wonder: how many of these new apartment investors will flood the market with fresh supply? Unlike single house where the construction has slowed to a halt, the new apartment tidal wave of supply continue to pile on. As such, this will pound the price down in both the re-sale sector and the rental market. For example, in Surrey, we are seeing a whooping 10 months of supply (for context, 4-6 months is balanced and healthy). Thus, apartment Buyers will have a great time in this oversupplied market, and it looks to stay that way in the foreseeable future. Interestingly, a trend that is flying under the radar is developers unlocking their fear of failed completions, many of which are from overstretched Buyers who jumped into the pre-sale frenzy many years ago. In order to gauge how many failed Buyers or bad debt they might take on, the developers are requesting early from Buyers their lawyer and bank financing info. One thing's for certain is that most developers will have a hard time selling their project at the same price now than they did 2-3 years ago. BC developers are faring much better than Toronto, where news of Toronto pre-sale Buyers have over 30% ratio of failure rate to complete. This is where it gets ugly really quick.

For the month of August, the best performing neighbourhoods for apartments were mainly in the outskirts of Burnaby North, Sunshine Coast and Vancouver East, at +0.4%, +0.2% and 0% respectively. Conversely, the areas with the most significant price drops were West Vancouver, North Vancouver and Tsawwassen, posting -3.4%, -3% and -2.9% respectively. The apartment and condo segment remained in a balanced market, with average days on market shooting up to 42 days (compared to 35 days in July). Month-to-month sale price continue to slip at -1.2% (compared to -0.6% in July). Sale-to-listing (% homes sold) ratio also slipped to 14% (compared to 15.9% in July).

|

2. Contraction & Recession

After months of the federal government insisting that the Canadian economy is resilient to tariffs, the latest print of GDP contraction of -1.6% annualized struck like a lightning. No matter what the government says, the recession is in the print, and more rate cuts will come. (Source: Bloomberg, Statistic Canada)

|

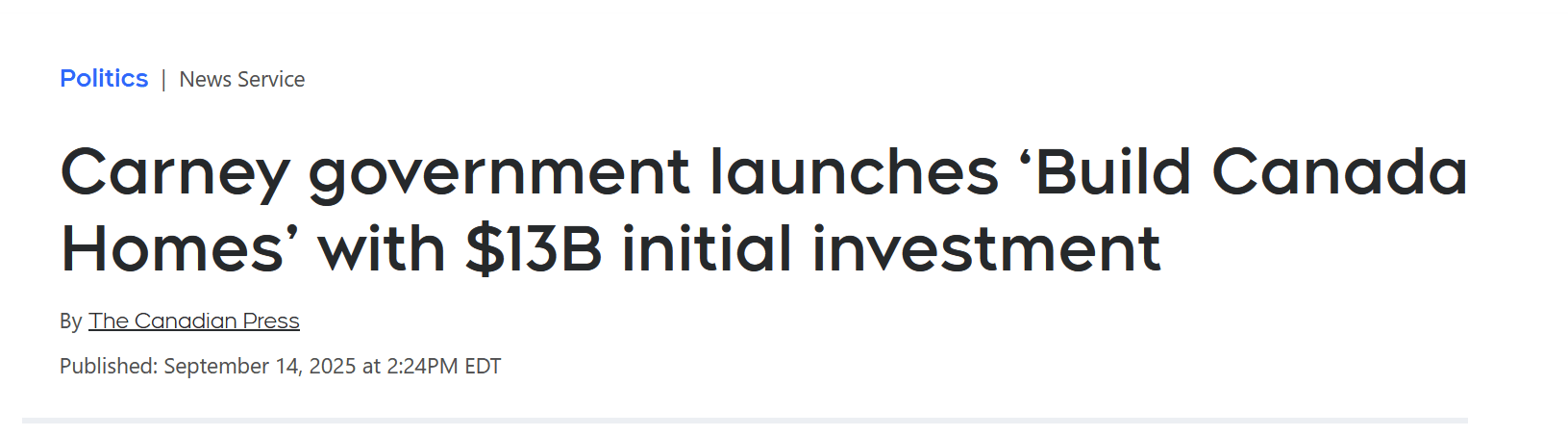

3. For Who?

"Build Canada Homes" by the Carney government is promising to build 4,000 units per year on federal land by partnering with developers. So these homes are all rental homes, and not a single word on the mounting social issue on affordability nor home ownership. So is forever renting the answer to the Canada's housing crisis? (Source: The Canadian Press)

Recent Posts

GET MORE INFORMATION