Real Estate Market Intelligence February 2026

Real Estate Market Intelligence

February 2026

A month into the new year and the surprising warm weather is already seeing some early cherry blossoms in BC. I was pleasantly surprised to have seen spotted two in Richmond. There was renewed optimism starting the new year, with reports including the from Greater Vancouver Realtor (formerly Real Estate Board of Greater Vancouver) stating that this year will have more sales than last. However, the new year in Vancouver real estate continues the same sluggish sales as last year, sending chills amid weak demand among Buyers. Lots to cover this month as Canada's January unemployment rate dropped to 6.5% by shedding 25,000 jobs, inflation edged down to 2.3% (from 2.4%) in January but food prices continue to rip, and the BC NDP government now prepares for the biggest financial deficit ever recorded.

The renewed optimism of kick starting the new year of Vancouver real estate was quickly squashed as January sales slump continues at -30.9% below the 10 year average. This is third slowest January in the past 25 years outside of 2009 (Global Financial Crisis) and 2023 (aftermath of massive interest rate hike to 5%). Seller, too, continue to jump into the market, with supply surging another +38% over the 10 year average. Again, the combined spread is 68.9%, which translates into further downward price pressure. The total listing-to-sales ratio (across all segments) are now sitting at 9%, which means only 9 out of 100 homes are sold, and 91 are unsold. One of the very noteworthy stat was the monthly price change, which was -1.2% in January across all segments. This was the a significant monthly decline, and if anything, looked to have accelerated in January. Anecdotally, there certainly is more buyers out there is in open houses and showings, but it has yet translated the increased traffic into more sales. This tells me the Canadian economy uncertainty is still lingering with the buyers. Thus, holding pattern remain high with most Buyers (i.e First Time Home Buyers who live with their parents). The weaker demand is the top straining factor, which is clogging up the entire real estate sales cycle. During the days of FOMO (Fear or Missing Out), buying first and then selling was easy. Now, most buyers who are looking to upsize need to sell first. They will no longer take the risk of buying first and sell. For this reason, there is no churn in the market when selling is so tough. To make matters worst, real estate investor remain nowhere to be seen. What was once a dominate driving force of the market share (nearly 30% investors) will have a significant impact on Vancouver real estate, especially in the condo segment and for those micro-homes under 500 square feet. Meanwhile, some Sellers continue to believe the mirage of Vancouver market recovery to be right around the corner. For the past 20 years, Vancouver real estate market slumps usually last 6-9 months, and this time its latest cycle has been 7 months since US tariff in April 2025. In fact, the last longer cycle of higher price point was in May 2024 (highest price point was March 2022). In other words, the current longer cycle has been running for 20 months. In my opinion, there's still more ways to go. I do believe that there will be a point where buyers and sellers reach a point of equilibrium, where prices meet demand, but this "point" heavily relies on any good economic news from Canada, one of which is is CUSMA (Canadian United States Mexico Agreement), which is up for joint review on July 1, 2026. If anything, this has the potential to make things better or worst for the Canadian economy.

As for the economy, the Bank of Canada's did what was widely expected to hold the interest rate at 2.25%. The opinions are getting polarized as I hear most economists predict the rates to go down further, but outlier like Bank of Nova Scotia has said the rate would go up. What I find more indicative would be the unemployment rate, which in January dropped to 6.5% by shedding 25,000 jobs. Looking closely, the manufacturing sector took a huge hit at losing 51,000 jobs since last year, with Ontario bearing the brunt. As per prime minister Mark Carney's words at World Economic Forum that the "Old world order is not coming back", and governor of Bank of Canada Tiff Macklem also chimed in that CUSMA, if not renewed, would take Canada into a recession, it is clear that Canada's path going forward to not put all the trading eggs into the US basket. Whether we like it or not, Carney struck an EV deal with China in exchange or canola, and "new world order" partnerships will be established, with old ones out the window. My view is that as the world swings further right into protectionism, loyalty is no longer cherished and friends and enemies can quickly change sides. By the same token, former enemies (Canada vs. China) are establishing new ties, but I remain cautious as any trade agreement with China should come with a caveat.

More economic updates as inflation rate dropped slightly to 2.3% (from 2.4%) in January. There are reports by major banks and economist stating that 2026 inflation should be a non-factor. I must disagree because so far I'm still seeing food prices being elevated, and Canadians are now ever more conscious of how their grocery money is spent. Lineups at food banks are reaching historic highs, and Salvation Army stating first time food bank users rose at a whooping 61%. As 2026 goes on, I am fully prepared for many more "unexpected" food inflation items, like beef, strawberries, ground coffee prices all rising out of control last year. Speaking of out of control, the BC NDP's budget may just be a last straw on the camel, with a projected historic deficit of $11.2 billion. Note that Premier David Eby inherited a budget surplus from John Horgan of $5.6 billion. That's a difference of $16.8 billion dollars. Just how badly can David Eby manage the finance? Worst is, 40% of that budget was spent on BC Healthcare, and yet, hospitals and emergency rooms wait times are at a record high: family doctors no longer taking in new patients. Some seniors are still doctor-less. So Mr.Eby, where did all that money go? There's no way to sugar coat this, and it looks like the BC economy, along the Vancouver real estate, are poised to get worst before it gets better.

Some of the unique trends I've been observing:

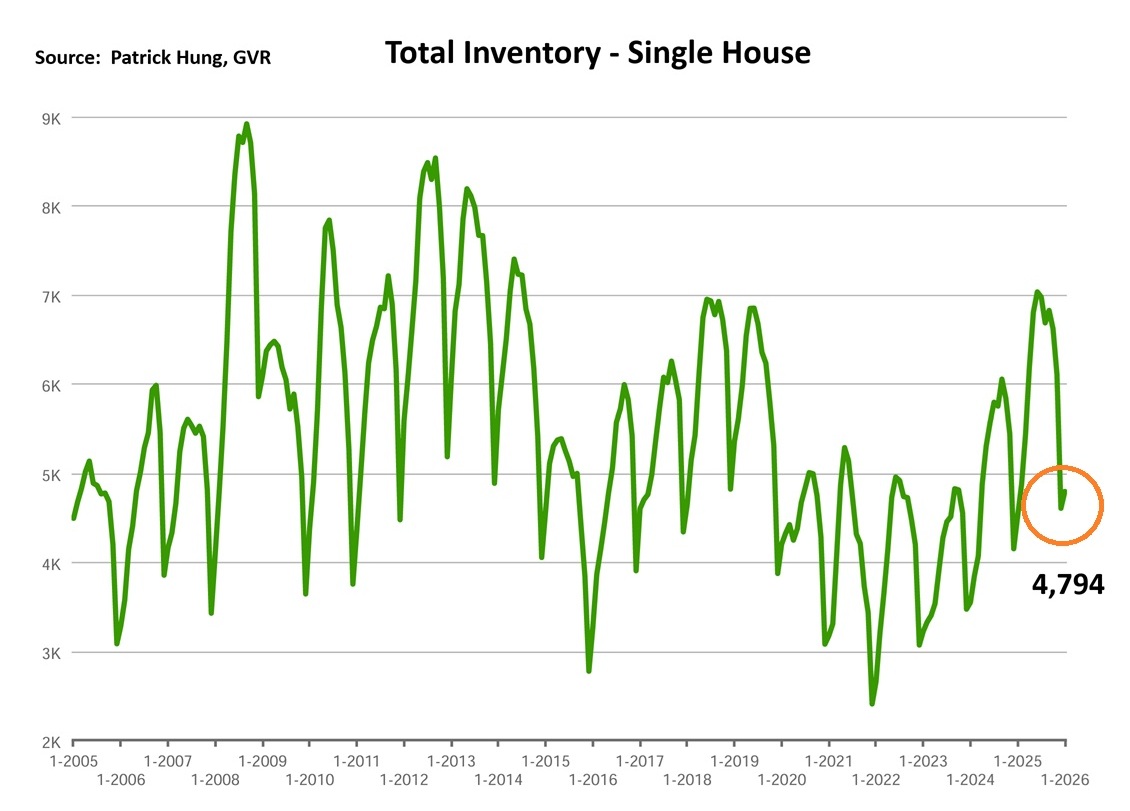

1. The Vancouver real estate market started off 2026 with the same results as last year. January had the third lowest sales for the month in the past 25 years, and supply was the highest supply for January in a decade. To put it into perspective, we currently have 11 months of inventory, and in a balanced market, that would be 5 months. We are now at over double of that in supply. It's evident that buyers continue to hold off in the face of uncertainty, and Sellers continue to jump in to liquidate. In the current market where Sellers need to sell first before buying, and when there's little to no buyers for their homes, there's simply no churn to the market. If one deal moves, three others move. Entry level homes are still in demand and can sell if priced sharply. However, lower price pressure remains for everything else. In my opinion, it will take a minimum of 6-9 months for the market to digest the current surplus in supply. That is, if the Canadian economy deteriorate further.

2. The Bank of Canada's held rates at 2.25% as wildly expected. Due to the weak economy, most economist are leaning towards another rate cut on the horizon. Would that move the needle and get some Buyers off the sidelines? Maybe, but the minor rate cut is more of a psychological boost than a financial one.

3. Despite the volatility, US stocks and commodities such as gold & silver prices continue to rip near record highs. Last year was pretty much a year without risk for these assets. On the contrarily, Canadian real estate in major cities like Toronto and Vancouver had one of the worst years. It wasn't hard to see why real estate investors have fled to scene, and it sure seems like it will continue that way.

4. Speaking of decade low real estate sales, did you know that 70% of real estate agents in Toronto and Vancouver did not register a single deal last year? In Vancouver alone, there's more than 1,000+ real estate agents quitting the industry altogether, which is approximately 6.6% of the pool of 15,200 agents back in January of 2025. The Greater Vancouver Realtor (formerly Greater Vancouver Real Estate Board) was not vocal about this as it could be detrimental to new agents looking to enter the industry. 2025 was the year of the great exodus amongst real estate agents, and 2026 looks like a continuation of that.

5. As the real estate trend remains in the Buyers' market, sales-to-listing ratio (% of homes sold) is sitting at 9% in January, which means only 9 out of 100 are sold, while the remaining 91 homes are sitting on the market. With that said, I've seen some great deals for Buyers, but the truly amazing deals were actually struck by the unadvertised ones. By that I mean they had to be discovered, such as the Seller's asking price may not be attractive, but the sold price was a jaw dropper of nearly reverting to 2021 levels. This tells me that some sellers' serious motivations was not openly disclosed, but it requires a low ball offer or two, and a lot of patience, to discover just that.

6. Rents in Canada has fallen for 16 consecutive months across all major provinces, with BC claiming -4.7%, followed by Alberta -4.3%, and Ontario -3.3%. Landlords now are facing the dilemma when their tenants leave; whether they sell with prices continue to trend down, or get a new tenant with possibly lower rent?

Here are the 3 highlights for January:

- Total inventory of 12,453 units is the fourth highest January's total inventory in the past 21 years. Sales continue to be weak while inventory piles up.

- There was a lot of noise and optimism about the real estate in 2026. They were quickly silenced by the continuing sluggish sales.

- Home prices had a monthly price drop of -1.2% in January, which is the most significant monthly drop in recent years. This brings the total of -2.2% price drop in the past 3 months. The weak Canadian economy continues to have a drag on the real estate market. As mentioned before, if Canadians are worried about lost their jobs, the last thing they would consider is purchasing real estate.

Here are the in-depth statistics of the January:

- Last month's sales were -30.9% below the 10 year January's sales average. This seem to have worsened since 3 months ago, and is continuing on that trajectory.

- Month by month residential home sales dropped by -38.5% from December 2025.

- Month by month new home listings shot up by +178.8 (not a typo), mainly due to many listings had expired and were relisted again in January. Also, some Sellers cancelled their listing back in the fall and elected to re-list in the new year, with a sense of renewed hope wishing for a better price.

- Last month's price dropped further by -1.2% (compared to -0.8% in December 2025)

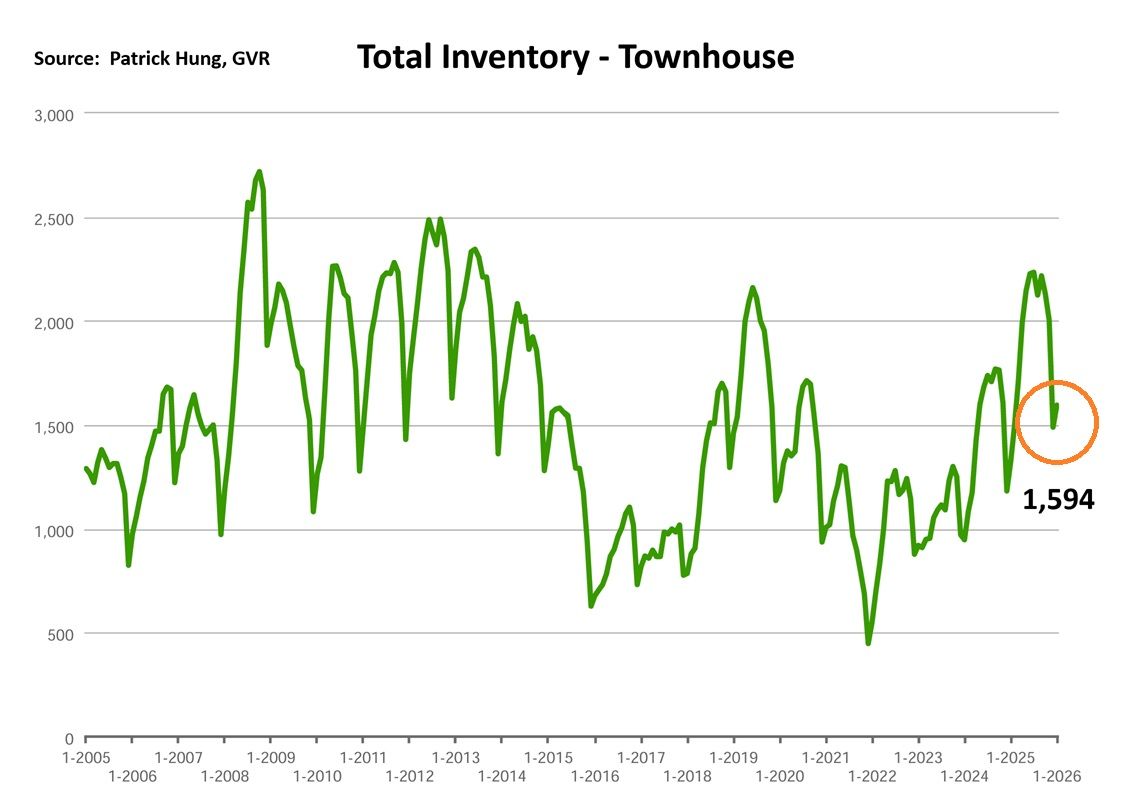

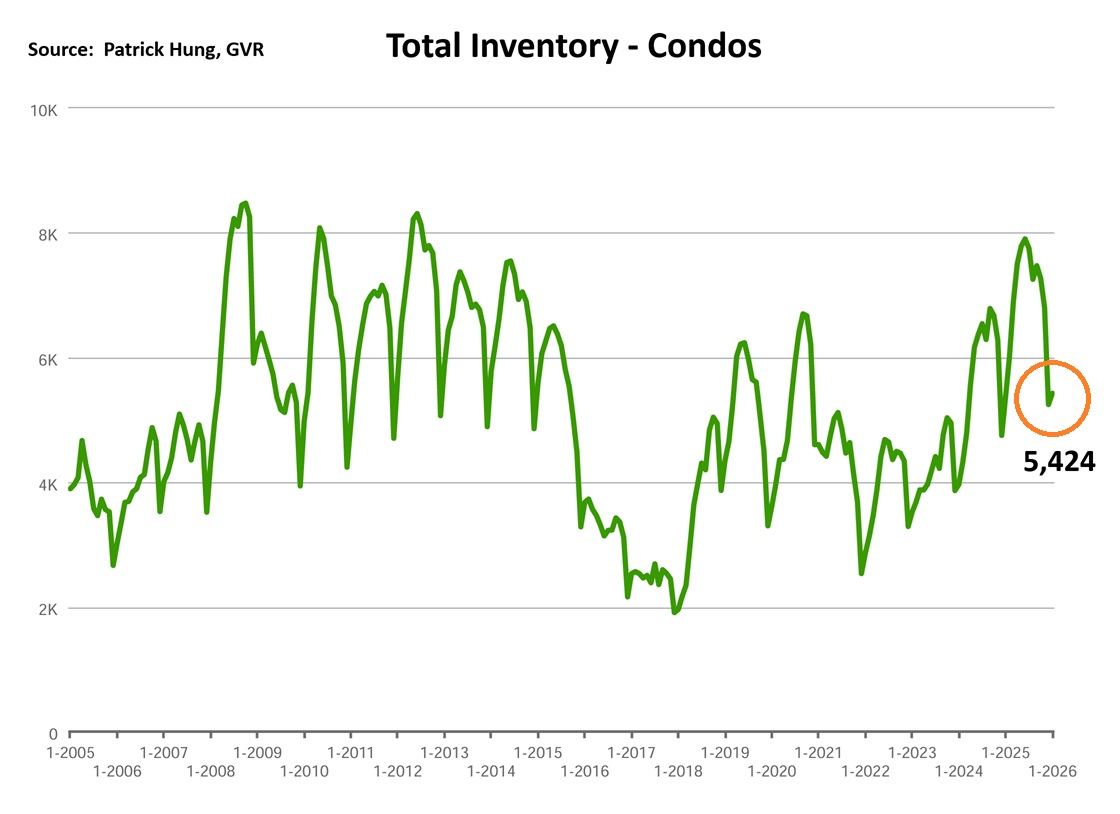

- Sales-to-listing (or % of homes sold) ratio is dropped significantly to 9.1% (compared 12.7% in December). By property type, the ratio is 6.7% for single houses, 11.1% for townhouses, and 10.3% for condos.

Download January 2026 Real Estate Market Report

Single House Market

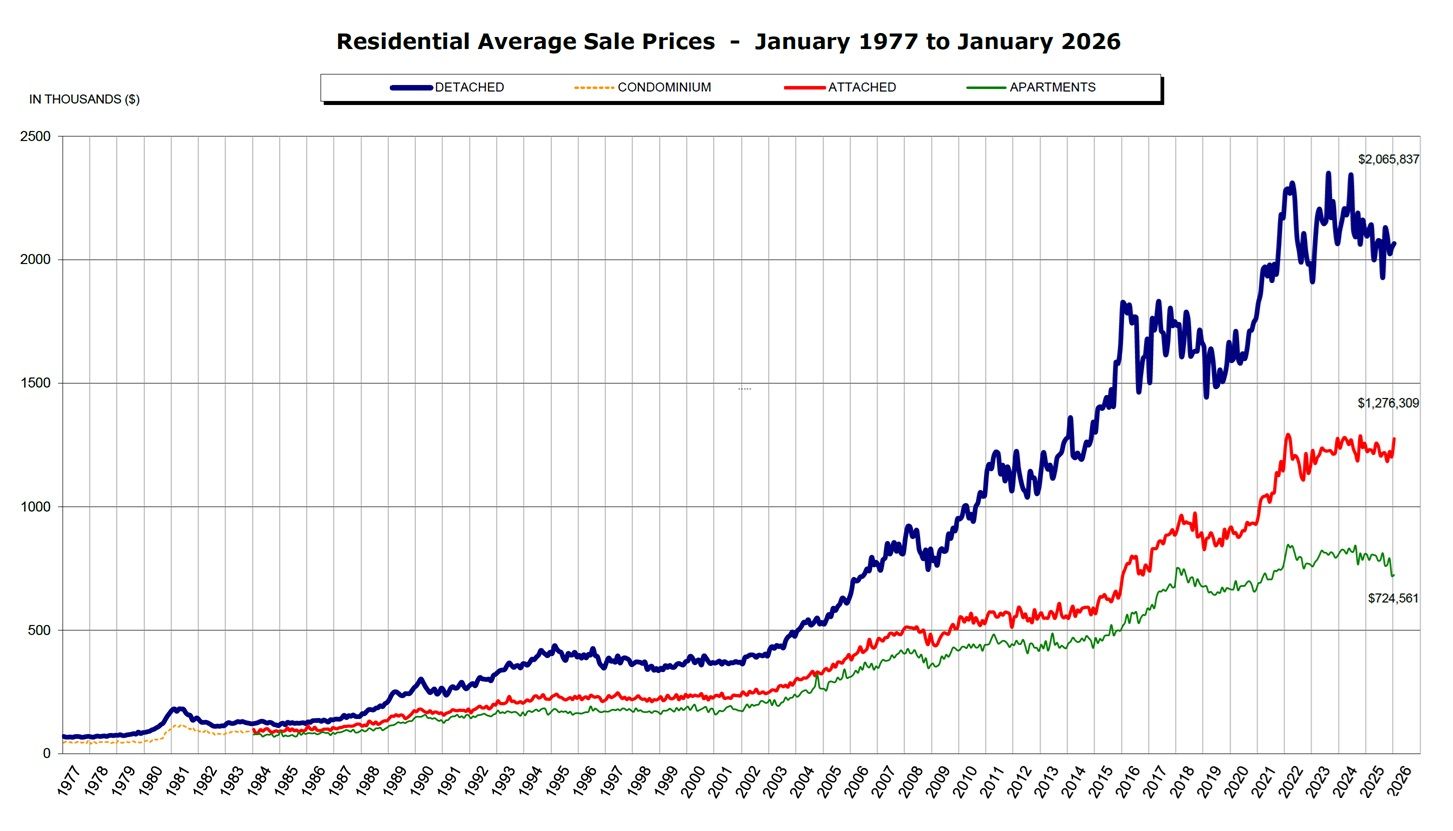

The single house market is started the new year veering heavily into the Buyer's market. The statistic that stood out was the single house sales to listing ratio (% of homes sold) sitting at 6.7%, which means merely 6.7 out of 100 homes are sold, and 93.3 homes are not sold. For the past few months, there is increased momentum in the downward price pressure for single houses, as this segment the most significant monthly price drop in January at -1.5%, which is the highest across all property types. To put that into the past few months monthly price drop only ranged between 0.6% - 0.8%, so January's sudden dip was double of that. On the streets level, this stats seems to be aligned correctly but mainly leaning towards homes that are in a below average neighborhood with a dilapidated home. However, homes that are in an ideal neighborhood, good practical layout that's well taken care of, these homes are still commanding near or above market price. The reality is, the market has more poorly conditioned homes that good ones, and when a poorly conditioned home sells for below market price, that has a drag on the entire market. Entry level homes are still in demand and generate much more traffic. However, the term "entry level" is being redefined as the market condition deteriorates. For example, $1.6m single house used to be entry level 8 month ago. Now it's $1.5m. This is definitely beneficial to Buyers as their budget remains constant, the market has opened up itself to more inventory. However, the recent low sales is a sign that even a lower bar of entry is not enough entice the Buyers to move into the market just yet. Buyers now are not looking for a good deal, but almost a "Best" deal. It's been 20 years since the tables have turned, and the Buyers are taking full advantage of it. Another sub-trend that I've observed is that premium homes $2-3m are having one of the lowest sales to listing ratio (% of homes sold) at 3%, and anything over $3m is even worst at 2% sales ratio. Simply put, the wealthy Buyers are even more sidelined than the average Buyer. No matter what tier the single homes are, the weakness is in the writing. Seeing that -1.5% price drop in January may be a blip on the map, but if this trend persists for a few months, it may be a sign of a major correction incoming.

For the month of January, the neighorhoods that registered most price growth were all in the outskirts, such as Whistler, Tsawwassen and Squamish, posting +5.9%, +4.9% and +4.7% respectively. Conversely, the neighborhoods registered the most significant price drops were Vancouver West, West Vancouver and Richmond, with -5.8%, -5.1%, and -2.2% respectively. The single house market dove deeper into the Buyers market, with average days on market remaining hitting higher at 61 days (compared to 59 days in December), and month-to-month average price dropped accelerated to -1.5% (compared to -1.1% in December). Sales-to-listing ratio (% of homes sold) dropped further to 6.7% (compared to 9.3% in December).

Townhouse Market

For the past month, the townhouse market seems to be caught perfectly between single house and apartments in terms of price decline (-1.2%). However, sales to listing ratio (% of homes sold) seem to be the best across all segments at 11.1% (compared to single house at 6.7% and apartment at 10.3%). Having said that, even the townhouse market, which was one of the most favorable property types, could not escape from being dragging into the Buyer's market. Historically, Greater Vancouver townhouses is always the least supplied property type, so it's easy for it to hoover between the Sellers and a balanced market. In my opinion, the weak townhouse sales was dragged on by the lackluster apartment sales. Why? Young Canadian families choose to upsize from apartment to townhouses due to their tighter budget. When these families are looking to sell their first apartment home, they can a lot of competition and cannot sell easily, and their plans of purchasing a townhouse gets pushed back. Given the abundant supply in apartments now and with more pre-sale constructions completing in 2026, I believe this drag into the townhouse will continue. Anecdotally, entry level townhouses around $800k in Greater Vancouver suburbs such as Richmond, Burnaby, Ladner, and East Vancouver are still performing fairly well. They may not sell within the first week, but are more likely to do so in the first few weeks, which in the current market conditions, is quite an achievement. On the contrarily, the Fraser Valley townhouse market, due to the healthy supply, is having a much harder time as more competitors pile on. These townhouses developments in Surrey and Langley are of greater scope (i.e 80+ townhouses complex) relative to Greater Vancouver's (i.e 20+ townhouse complex). Plus, the Fraser Valley has a faster development turnaround time (1-1.5 years) compared to Vancouver's (2-3 years). Thus, the speed of these projects from idea to construction to sales is faster, and can easily meet the demand in a tight market, but flood the market in an oversupply market. On a side note, one of the unique trends I'm also observing is that brand new Metro Vancouver townhouses (i.e Westside) are getting squeezed out of the market by the new multi-plexes (3-8 unit homes on a single lot). The advantages of these new multiplex homes are threefold: 1./ They can be situated in more a quiet street (compared to most townhouse projects that on arterial roads like Granville and Oak), and 2./ More competitively price in terms of price per square foot, and 3./ Not needing to pay strata fee, which most Buyers are not fond of. The major disadvantage, though, would be the lack of parking space. Some don't even have one. Either way, townhouse will face similar competition, but this segment faces a newcoming competitor: multiplex. And so far, this competitor is winning a good slice of the market share.

In January, the areas with the most townhouse price growths were mainly in the outskirts in North Vancouver, Pitt Meadows, and Vancouver East, registering +1% (tied for 1st and 2nd), and +0.2% respectively. Conversely, the neighborhoods with the most significant price drops were Burnaby East, Burnaby South and Maple Ridge, at -6.1%, -3.8% and -2.5% respectively. For the first time in a long time, the townhouse market has shifted into the Buyers market, with days on market jumping to 47 days (compared to 42 days in December). Month-to-month sale price declined further to -1.2% (compared to -0.9% in December). Sale-to-listing (% homes sold) ratio dropped to 11.1% (compared to 14.6% in December).

Condo Market

On the surface, the condo market price had the least price decline (-0.8%) across all segments last month (compared to single house -1.5% and townhouse -1.2%). Diving deeper, we're seeing a deeper structural change in the condo market, which is the shadow inventory (pre-sale supply that's not sold) and is completing in 2026. At the moment, we are only seeing a slower decline in condo prices, but I predict that as the year goes on, the condo supply may very likely hit reach a record high due to the influx of the shadow inventory becoming available. This would further cause prices decline to accelerate. One of the things that also affects the condo segment is immigration, where major provinces like BC and Ontario are seeing a net outflow of residents. With less people living in Vancouver now that last year, the economy (including real estate and rent) would either be stagnant or going downhill. Condo market was once the darling of the investor's market, but with nearly all investors escaping the scene, demand will continue to diminish when compounded with declining population. Either renting or selling, condo prices will face the most challenges this year across all segments.

For the month of January, the best performing neighbourhoods for condos were in West Vancouver, Tsawwassen and Ladner, at +7.6%, +4.1% and +3.8% respectively. Conversely, the areas with the most significant price drops were mainly in New Westminster, Sunshine Coast and Squamish, posting -3.6%, -3.2% and -2.6% respectively. The condo segment shifted into the Buyers market, with average days on market increasing to 49 days (compared to 48 days in December). Month-to-month sale price slipped the least of all segments at -0.8% (compared to -0.6% in December). Sale-to-listing (% homes sold) ratio dropped significantly to 10.3% (compared to 15.1% in December).

Here are the Three Trends I'm Observing:

1. Downward Spiral

Rents in Canada has declined for 16 consecutive months, as rents fell across all major provinces, with BC claiming the steepest drop at -4.7%, followed by Alberta (-4.3%) and Ontario (-3.3%). With Canada's immigration all but stopped, compounded by a weak economy, there just doesn't look a recovery is on the horizon in rental prices anytime soon. (Source: Rentals.ca)

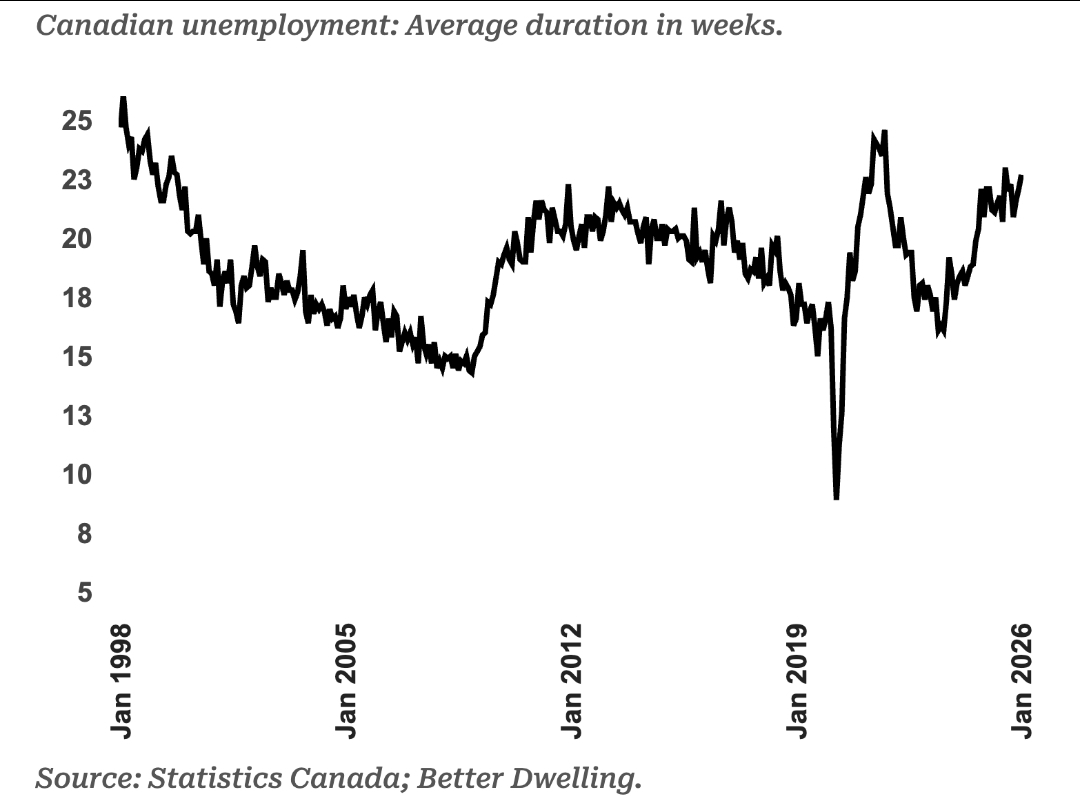

2. 23 Weeks Later

On the surface, the latest unemployment rate at 6.5% is an improvement. Diving deeper, the average duration of unemployment between jobs has jumped to 23 weeks, which is the highest since 1999 outside of the pandemic. Along the same lines as Canadian emergency room wait times are now much longer, some unemployed Canadians are also dying of impatience to get back to work. (Source: Statistic Canada, Better Dwelling)

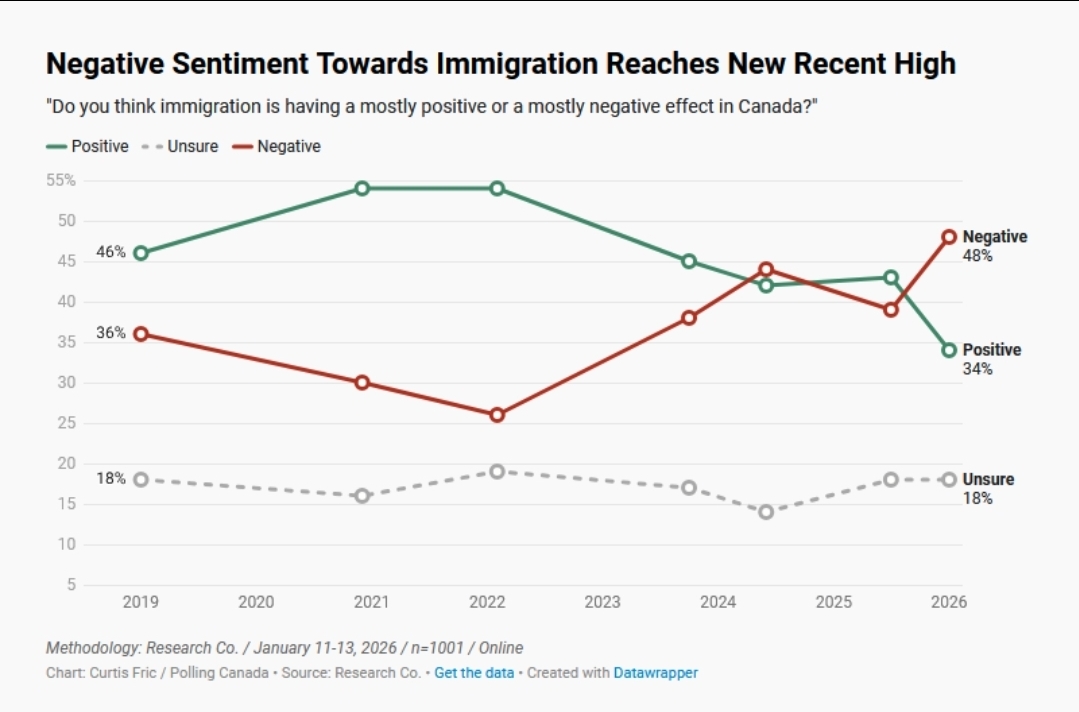

3. Hard Right

In one of the worst immigration policies imposed by the Trudeau era of letting in 3 million immigrants (roughly 7.5% of the entire Canadian population) in 3 years, we are now witnessing the aftermath. Negative sentiments towards immigrants are now reaching highs of 48%. Canadians feel the infrastructures from roads, schools, hospitals, to kids playgrounds are being overwhelmed. Just how can any country let in 3 million people without any plans or improvements to infrastructure? Also, temporarily workers continue to compete in same space as most young workers do, causing unemployment rate to rise the highest amongst youth between 18-25 years old. Canadian immigration is poised for swing to a hard right. As doors will remain shut in the near future, the Canadian economy is will also have harder time to grow with less people in it. (Source: Polling Canada, Research Co.)

Recent Posts

GET MORE INFORMATION