Real Estate Market Intelligence November 2025

Real Estate Market Intelligence

November 2025

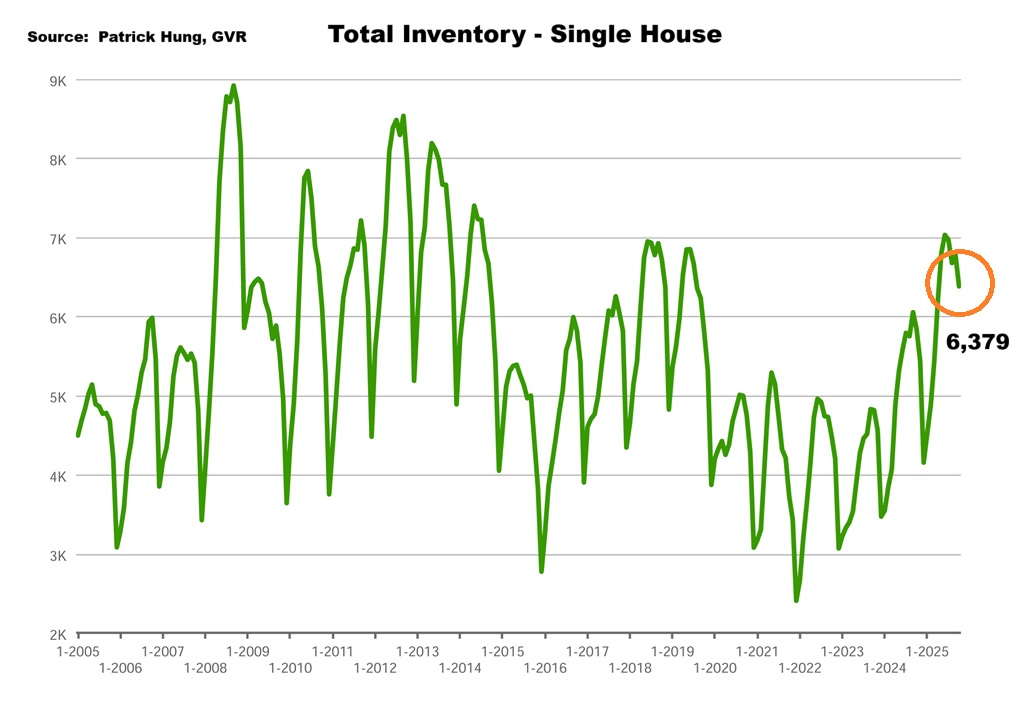

Fall is in full swing and Vancouver has been blessed with a sunny and dry November thus far. As most Vancouverites are pleasantly surprised with the weather and with more outdoor activities, the real estate market saw an uptick in sales October as well, albeit it is still -14.5% below 10-year average. I've been emphasizing for a long time the importance of the first month of the last quarter of 2025, as it's sets the tone for the remainder of the year, and possibly into the New Year. Looking closely, last month was the 4th slowest October sales in the past 10 years. It wasn't that bad, right? On the surface it might look that way, but in reality it was only behind major events such as 2019 (introduction of speculation tax, reduced foreign investment) and 2022/23 (higher interest rate era). This time around, the tariff is exposing the structural weakness in the Canadian economy that is trickling into the real estate. The key component I've been stressing over the years in Vancouver real estate is the supply, which in October is sitting at 15,976 units and is a 12 year high for the month. When we compound that with over 4.1 million immigrants admitted over that period PLUS the unknown number (yet an explosive amount) of non-residents and temp works over that same time, we can now feel the weakness in the demand, or how affordable, the Vancouver real estate market has become. Lots to cover this month as we explore Canada's surprising drop of unemployment rate to 6.9%, the federal government's fiscal deficit of $78.2 billion, and the massive First Nation Cowichan land claim that has rocked the nation.

The October Vancouver real estate market sang similar tunes to the late summer months; sales drifting around 15-20% below 10 year average, while inventory is at a decade high. Despite the increased sales, the October numbers are still abysmal. Elevated inventory continues to push prices lower as the Canadian economy weakens. Even in times of the winter months where listings are usually lower, we are seeing over 15,976 units of total inventory in Greater Vancouver, which is nearly 4,000 units (or 33%) over the 10 year average for monthly inventory. This continues to apply further price pressure on the current inventory, with no end in sight for the near future. Anecdotally and speaking with many buyers at open houses, almost ALL of them are looking for good deals. For those Buyers who are ready and willing but does not have urgent need (i.e First time home buyers living with parents), they are still playing the waiting game. As prices continue to decline, we are seeing more Sellers getting desperate for a sale before year end. Why? Keep in mind that the latest BC government assessment comes out at end of the year, and this year looks certain to have a significant correction. When that does, both Buyers' and Sellers' mentality will change. Thus, some Sellers who have the foresight is seriously looking to liquidate will slash their prices. In doing so, it causes a ripple effect into the homes in the area. Once the lower priced home is sold, it becomes the benchmark for other Buyers to compare. By the same token, we are seeing frustrated Sellers cancelling listings in Greater Vancouver running at double the levels seen over the past few years. My observation: Sellers either seriously consider selling now, or cancel and wait till the market recovers (which who knows when this would happen).

As for the economy, the Bank of Canada's latest rate cut of another 0.25% brings the overnight rate to 2.25%, which is at the lower end of the neutral rate. Any further rate cuts would be considered as stimulative and as signs of economic deterioration. I personally think the Bank of Canada will hold out for at least 3 more months for more clarity. As for the inflation, it has surprisingly jumped up to 2.4% in September (from 1.9% the month before), and among that CPI basket, the shelter inflation cost was kept in check as -0.1% decrease. One of the most important items, food, has seen inflation shot up by 4% from last year. There was some good news given that the unemployment rate has dropped to 6.9% (from 7.1% the month before). This time around, it added another 66,000 jobs. Remember it was only in July and August that we had 7.1% unemployment rate and we lost 100,000 jobs? It is exactly these wild fluctuations that keep me skeptical of the job data. As for much delayed Federal government's fiscal budget, the Carney government have managed to rack up $78.2 billion deficit, which is the second largest in history. Still, the federal government insists Canada is the best among G7 countries. In my opinion, that's like bragging about being the last person in a sinking ship. Whether we like it or not, Canada needs to save itself from the over-reliance on US. On top on that, we are the ONLY country that has not reached an agreement over the US tariff. Carney has made it all along his campaign that it would be his first priority, yet we are dead last.

Last but not least, the Cowichan land claim in Richmond that has rocked the nation is gaining traction globally, as I don't see any signs of it going away soon. Being a Richmond resident myself, I having spoken with multiple lawyers about the matter and the judge's ruling of the claims of the land being "unceded", meaning the First Nations never surrendered the land, aka land has not reached an agreement, can now theoretically have two titles; one fee simple (private land), other being under the Cowichan title. In reality, this cannot happen because banks will not recognize two titles on the same land. Talks of residents affected in the Cowichan claimed area have confirmed that their banks have denied renewal of their mortgage. Also, they cannot sell their land. What options do they have when they cannot refinance nor sell? Worst yet, the Richmond mayor, Malcolm Brodie, has been confirmed that he had knowledge of such a claim back in 2014, only to undercover this matter this year (which happened he had declared that this year to be his last year in office. Coincidence?) Either way, we've only at the tip of the iceberg as it was again recently revealed that the entire city of Kamloops, with population 111,499, is now under the land claim. Needless to say, the latest ruling will put the entire Canada's private land system in danger. This has become such a political mess yet the federal government have not responded to it. I strongly believe that the negotiations are happening behind closed door (which have been the case in Richmond for over a decade), and the government will let the noise die down a little. This is one of those things that will continue to haunt many Canadians, especially those in British Columbia.

Globally, both the stock and gold markets are starting to come off their highs in late October. As Canada's interest rate now is reaching it's lower limit, would the real estate Buyers now seriously consider making that lateral movement, cashing in on their investment gains in the past 6 months and jumping into real estate market? With their substantial investment gains over the last few months, the Buyers' downpayment have increased and so has their purchasing power, while the real estate prices have been falling at the same time. We haven't seen this divergence in a long time, and when looking at it from a Sellers' perspective, they see the value of the hard asset of their homes fall while the investment market going to the moon. This would furthermore motivate the Sellers to liquidate and possibly lower the listing prices further, with Buyers picking up the deals. Typically, November is the month to kick start all the retail shopping frenzy, while at the same time the beginning of the slowdown of real estate sales, but keep in mind that this year has been anything but typical. Beginning this November, I have been seeing some aggressively priced homes starting to attract unintended multiple offers. Could this be a sign of things to come? Let's see.

Some of the unique trends I've been observing:

1. The Vancouver real estate market in October was still slow but came out better than expected, with sales -14.5% below the 10 year average. On the other hand, the total inventory has remained high at +35.9% above the 10 year average. In other words, the spread between the sales and demand is sitting at 50.4%, which has been hoovering around the same mark for the past two months. Noteworthy was that in June, the spread once hit a high close to 80%. In June, that was a 30 year low in sales. And now, it's a 10 year low. In other words, the Vancouver market has gone from worst to bad. Either way, it still doesn't look good.

2. The Bank of Canada's rate cut of another 0.25% isn't moving the needle. As we are now at the lower end of the neutral rate, it is very unlikely for the Bank to further cut rates as it would prove to be stimulative. Having known that this rate cut cycle is at or near its end, would that motivate the real estate Buyers to finally come off the sidelines?

3. One of Canada's key economic indicator is the unemployment rate, which in October surprisingly drop to 6.9% (from 7.1% from the month before) by adding 67,000 jobs. I continue to be skeptical about the number provided by Statistic Canada, given that volatility of the jobs data (October 67,000 jobs added, September 66,000 jobs added, July + August over 100,000 jobs slashed). I feel the economy is much weaker than what's reported now as I hear more hiring freeze and layoffs rather than optimistic companies and workers.

4. The Cowichan land claim ruling in Richmond has rocked Canada and places the entire fee simple (private land) system under fire. Residents affected in the area has confirmed that they can either renew their mortgages nor sell their home. As the story continue to unravel, I believe negotiations with the First Nations are and will happen behind closed door. While the federal and provincial government remain silent on the matter, this issue is a swinging door that will keep coming back to haunt Canadians. The latest claim that was "released" is for Kamloops, a population of 111,499. So who's next?

5. Work from home is nearing an end as layoffs increase and the ball is now back on the employers' field. This has huge implications on suburban real estate (i.e Langley, Surrey, Maple Ridge).

Here are the 3 highlights for September:

- Total inventory of 16,393 units is the fourth highest October total inventory since 2013. Sales and demand has increased, but inventory and supply continue to outpace the demand.

- Many Sellers are looking to close out the year with a sale, and has reduced their price accordingly. This has created much more attractive deals and Buyers are starting to come off the sidelines. In some cases, this has created unintended multiple offers.

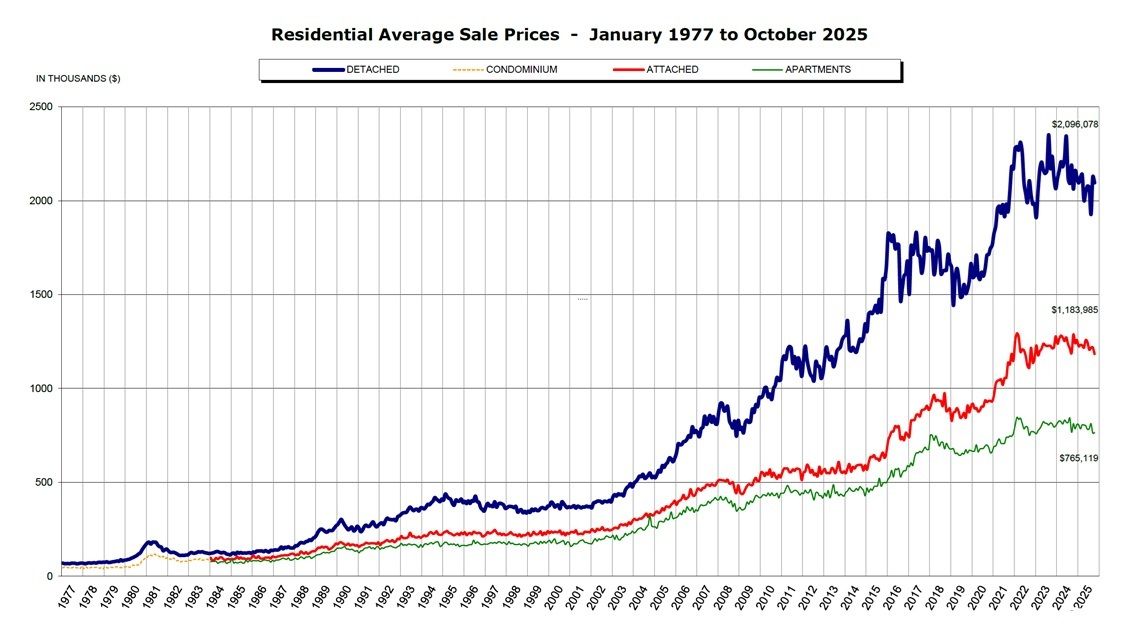

- Home prices continue to slip, with average monthly price dropped by -0.8%, and by a total of -3% in the past 3 months. The 3-month price drop came from apartment (-3.3%), townhouse (-2.9%) and single houses (-2.9%).

Here are the in-depth statistics of the September:

- Last month's sales were -15.9% below the 10 year October's sales average. This was an improvement compared to -20.1% in September. Prices have come down to a point where Buyers feel they are acceptable.

- Month by month residential home sales shot up by +17.4% from September 2025.

- Month by month new home listings dropped significantly by +19.9% (compared to +35.1% compared to September 2025.) Some Sellers have elected to cancel their listings and try again in the new year.

- Last month's price dropped further by -0.8% (compared to -0.7% in September 2025)

- Sales-to-listing (or % of homes sold) ratio is increased slightly to 14.2% (compared 11.3% in September). By property type, the ratio is 11.3% for single houses, 17.6% for townhouses, and 15.5% for condos.

Download October 2025 Greater Vancouver Real Estate Report

Single House Market

Since the beginning of October and up until mid-November, we are seeing the single house market showing signs of increased traffic and increased sales. Of course, this is for those that are competitively priced. Month-over-month sales shot up +20.4% in October, and at the same time, the total inventory went down by -6.2%. For this particular sector, the price cuts are deeper, with a wide range from $100,000 to $900,000 at times. Having been holding out for the past 6-12 months, many single house Sellers come to their sense; either take a steep price cut now, or endure more price drop with no certainty in sight. The thought of losing another $100,000-$200,000 was enough to take them to consider what was once a lowball offer. On the other hand, more Buyers are now actively looking for a good deal, but remains hesitant when they see one. Anecdotally, I have a new listing came out in early November for a Eastside Vancouver Special, which is a 2 level with rentals possible on each floor. This type of property is always popular due to it limited quantities (don't make them anymore) and is an ideal mortgage helper or investment. At its peak in March 2022, such homes can command upward of $1.8m. My listing was in original condition so lots of work had to be done, and we had listed it competitively at $1.49m due to the renovations required. We were pleasantly surprised that we have 82 groups through our first open house, with an accepted offer secured 24 hours after. Colleagues of mine have also mentioned that homes that are competitively priced are getting unintended multiple offers. As the single house prices have dropped to a point where the Buyers acknowledge they are a good deal, it is only a matter of when who pulls the trigger. Key is, if 1 out of 10 of these competitively listings were sold, it would have a ripple effect on the remains 9 listings' values. More and more buyers are now circling around like vultures, yet they remain in deep fear of overpaying.

For the month of October, the neighorhoods that registered most price growth West Vancouver, Vancouver West and Port Coquitlam, posting +0.7%, +0.4% and +0.2% respectively. Conversely, the neighborhoods registered the most significant price drops were Pitt Meadows, Whistler, Tsawwassen and Burnaby East, with -6.1%, -4.2%, and -3.6% respectively. The single house market continues to be in a Buyers market for the tenth consecutive month, with average days on market remaining nearly flat at 46 days (compared to 47 days in September), and month-to-month average price dropped to -0.9% (same as September). Sales-to-listing ratio (% of homes sold) shot up to 11.3% (compared to 8.5% in September).

Townhouse Market

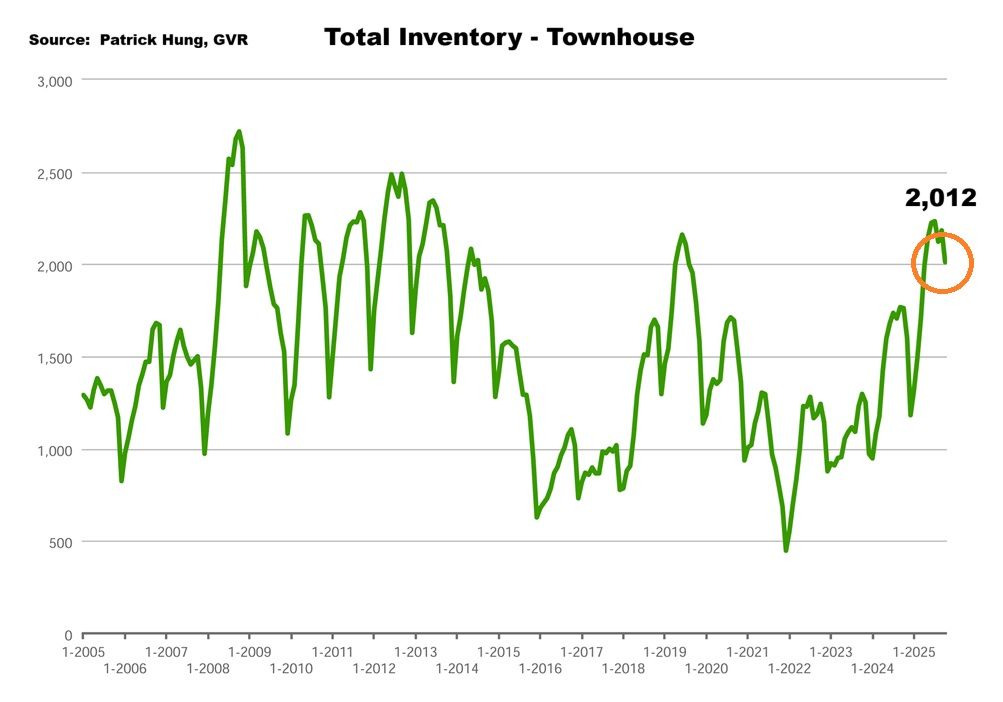

Of all property types, the townhouse market monthly price drop of -0.3% was the least (single house -0.9%, condo -1.4%). Townhouse's 3 month price adjustment is also mirror that of the single house at -2.9%. Month-over-month sales has shot up significantly at +27.8%, while total inventory dropped by -8.3%. In the current market where nearly all Buyers are end-users, the townhouses Buyers which consists of upsizers and first time home buyers see the prices drops are beginning to make sense to pull the trigger, especially before the end of the year. One thing is keep in mind that townhouse Sellers (young families) are those usually looking to upsize to a single house. So, if they see a good deal on the single house (where they save more), then they are more willing to lower their asking price or take a lower priced offer to make it happen. In other words, when the math makes sense for the townhouse Sellers to upsize, they don't mind taking a hit on the selling side, as long as they've gained more on the buying side. The lower rates, which is at the end of its cycle, seems to have driven some sales as well, even though they are more psychological than financial. With foot on the ground, I feel the townhouse price drop is greater than posted that of -0.3% last month, but again, same thing is true for the single house market, which in return the townhouse Buyers consider beneficial to them. Either way, the townhouse market is the best performing segment across the board.

In October, the areas with the most townhouse price growths were mainly in the outskirts in Squamish, Whistler, and Richmond, registering +1.6%, +1.4%, and +0.6% respectively. Conversely, the neighborhoods with the most significant price drops were Burnaby East, Pitt Meadows and Port Coquitlam, at -3.2%, -1.9% and -1.7% respectively. The townhouse market remained in a balanced market, with days on market nearly flat at 35 days (compared to 36 days in September). Month-to-month sale price dropped significantly by -0.3% (compared to -0.9% in September). Sale-to-listing (% homes sold) ratio shot up significantly to 17.6% (compared to 12.7% in September).

Condo Market

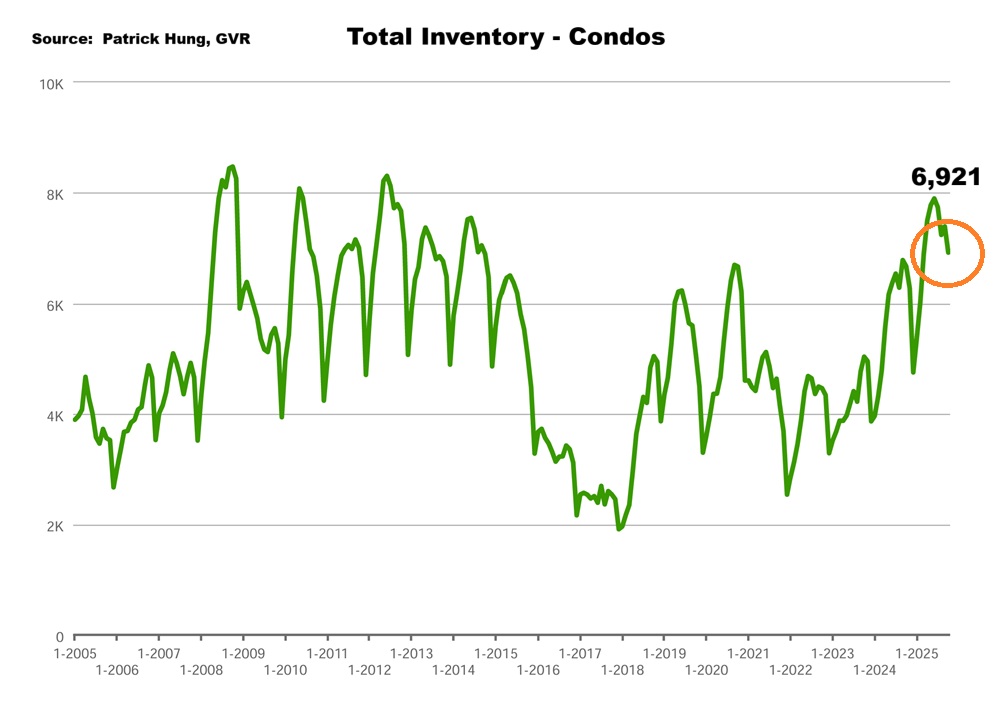

What can I say? The condo market has been, by far, the most volatile segment throughout nearly the entire year. From multiple decade high inventory to slowest sales in recent memory, it has absolutely fallen from its glorious times only a few years ago. In short, the October market for condo sales has gone up +11.7% while total inventory dropped by -6.7%. Sounds good, right? Not really, as it still remains the weakest spread of 18.3% between sales and demand and is the weakest among all segments. The condo segments just can't seem to catch a break, mainly thanks to the federal government's "success" in the rental houses program, which is having a massive supply surge and driving out all investor in the condo segment. Keep in mind that condo is one of the favourite type of investment for mom-and-pop investors, which has all but vanished these past two year. Without them, a core group of the buyers are gone, and to exasperate the problem, the surge in government rental supply keeps pushing the rent lower, which all but killed the pre-sale market even more. All the one-bedroom that's sub 550 sf are underwater, while the larger 2 bedroom condo prices are budding up close to an entry level townhouse. This certainly is one of the toughest time for developers, as they have been so used to bossing the market and bullying all buyers for over two decades. At once point in the peak of 2021-2022, a 3 month average of pre-sale was over 3000 units. Now? 300 units, which is a 90% drop in sales. If this continues for another year or two, it's safe to say that games are over for developers. It's an understatement that pre-sales are on life support, and that weakness in demand is resonating throughout the entire condo segment. Again, I don't see how this would recover anytime soon, given the direction the federal government's rental program is going to completely put the segment to sleep. Neigborhoods from far and wide, from Surrey, Langley, Brentwood, Richmond, River District, to downtown Calgary and Toronto, there is no escape. A cleansing is coming to condos: buckle up as we are in for a long ride.

For the month of October, the best performing neighbourhoods for condos were in Sunshine Coast, Port Moody and Whistler, at +4.6%, +2.4% and +2.3% respectively. Conversely, the areas with the most significant price drops were mainly in the outskirts in West Vancouver, Vancouver East and Vancouver West, posting -8%, -3.2% and -2.3% respectively. The condo segment remained in a balanced market, with average days on market increasing to 38 days (compared to 36 days in September). Month-to-month sale price slipped the most of all segments at -1.4% (compared to -0.7% in September). Sale-to-listing (% homes sold) ratio also increased to 15.5% (compared to 13.3% in September).

Here are the Three Trends I'm Observing:

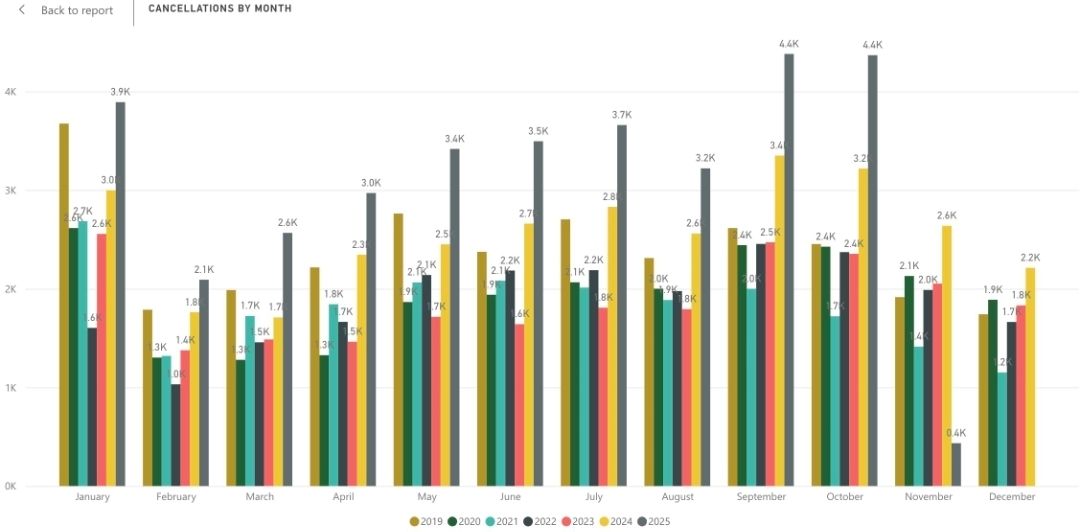

1. Cancel Culture

For over two decades, the real estate Sellers have been bossing the Greater Vancouver market. This year, the tides have turned and the Sellers are now being bossed around. As such, cancelled listings are now running at double of that in the past few years. With the current decade high inventory, only Sellers who are motivated will sell; many who are unhappy and with low motivation have decided to quit with the hopes to re-list when the market recovers. (Source: Greater Vancouver Realtor)

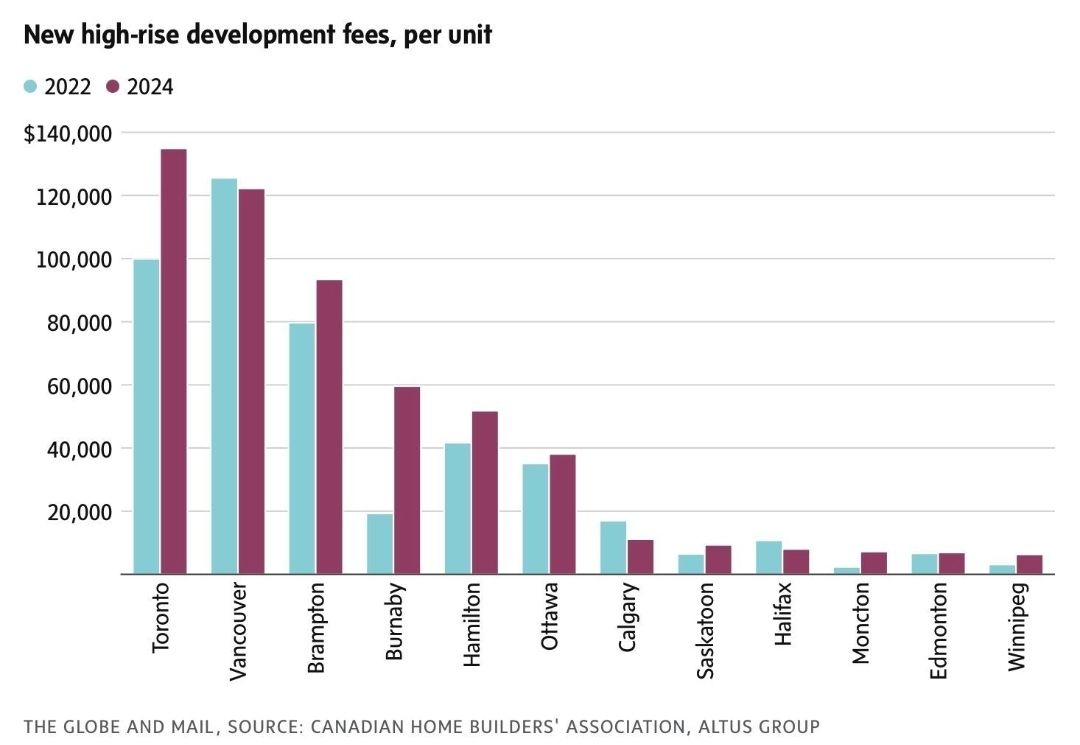

2. Development Fees = Development Freeze

Why is the Vancouver and Toronto new development and pre-sale market on life support? Well, look no further to the municipal governments fees (cash grab). Per unit, Toronto's development fee has rocketed over $130,000, and Vancouver is right behind at $120,000. On the other end, Winnepeg's is less than $5,000, Calgary is less than $10,000. This is another perfect illustration of the Laffer curve, where taxes have elevated to a point where it becomes unprofitable for developers to build, and the government ended up collecting less taxes with less projects and higher unemployment. In simple terms, taxes kill investments. (Source: The Global and Mail, Canadian Home Builders Association, Altus Group)

3. Own Nothing

The Carney government's latest released fiscal budget to "Build Canada Homes" is going all-in on rental housing, with no mentioning ofaffordability. The federal housing minister, Greg Robertson (formerly Vancouver mayor), in May said that home price should NOT go down, but the way to go is delivering more affordable (rental) housing. In other words, the Carney housing policy is similar to the saying: "Own Nothing and You Will Be Happy." (Source: The Canadian Press)

Recent Posts

GET MORE INFORMATION