Real Estate Market Intelligence March 2026

Spring is here; days are longer and flowers are blooming. It is hard to imagine it has only a little over two months into 2026, and the geopolitical tension has risen to decade high. So far, we have witnessed unrest in Mexico, Cuba, Venezuela, and now, the war in Iran and the Middle East. This new norm has created uneasiness with many, though such feelings may not be expressed openly. For the Vancouver real estate, Buyers and Sellers are also embracing a new norm: consistently low sales with elevated inventory. For the past 3 months, sales have been stuck around -30% below the 10 year average, while the total inventory being +33% above the 10 year average. The spread was roughly 60% and this has applied continuous downward price pressure, though in February that seemed to have eased a bit. Lots to cover this month as we explore Bank of Canada rate next announcement on March 18, which is widely expected to be another sleeper with no change. With the war in the Middle East causing oil to fluctuate wildly everyday, inflation is poised to shoot up globally, and how would that affect our interest rate and possibly the real estate market? Last but not least, the Canadian government had signed an acknowledgement with First Nation Musqueam Band recognizing aboriginal title over area covering much of Metro Vancouver, but had done so in secrecy and wasn't published by mainstream media until later.

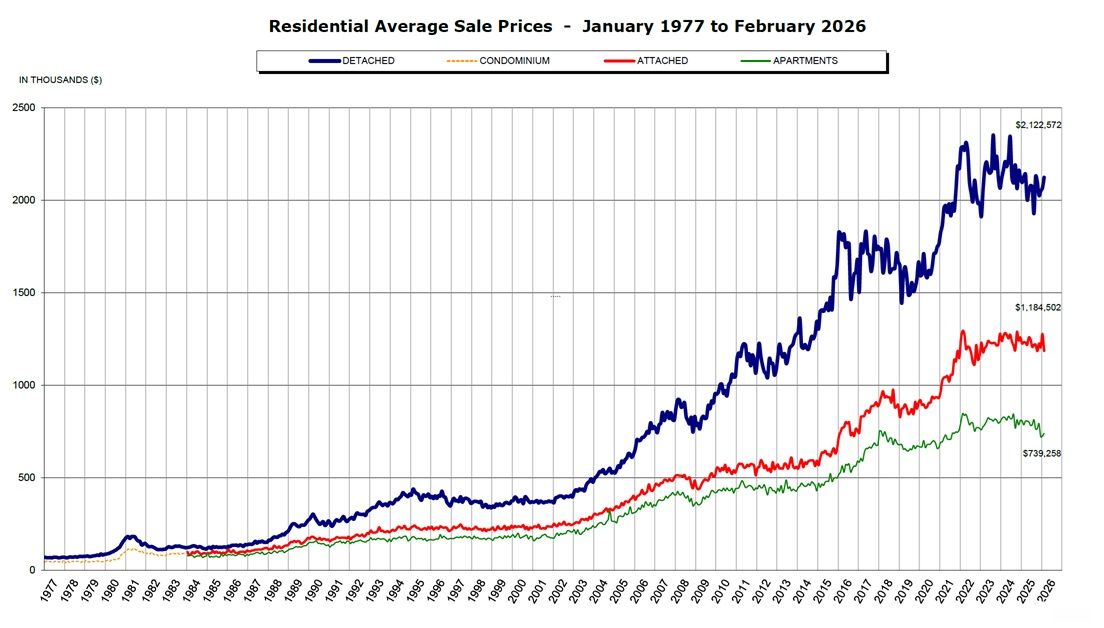

Last month, the Greater Vancouver real estate registered the 3rd lowest sales for the month of February in the past 25 years, with slowest February being in 2009 (Global Financial Crisis) followed by 2019 (Aftermath of heightened mortgage stress test and overseas buyer tax). On the bright side, the pace of the price drop has slowed, with monthly benchmark price dropping only slightly by -0.2% (compared to -1.2% in January 2026). Digging deeper, only the single house segment registered a price drop of -0.8%, with townhouse and condos prices rebounding at +0.2% and +0.5% respectively. It was also the first time in over six months that saw a price recovery in townhouse and condo segment. Total supply remains elevated, although it is worth noting that some Sellers have elected to take de-list their homes and try again later, while a minority of the Sellers are going all in and is committed to sell. Such divergence in Sellers' psyche was not evident only a few months ago, and it seems like the new year has created the environment where some Seller are more determined to liquidating than others. For the first two weeks of February, sales along with open house traffic was really slow. However, the last two weeks were busier as traffic picked as with increased sales came from a greater pool of listings carrying some better quality homes. Even with heightened uncertainty in the background, real estate remain a core human need that needs to be met. Family plans such as the need for more space with a second child, or a retiree who needs to go into a care home, or an estate sale, are all highly motivated plans. In the current market, it is exactly these highly motivated buyers (not investors) that transact with other like-minded highly motivated Sellers. Ironically and on the flip side, all the less motivated buyers (i.e renters with low rents, or first time home buyer living with parents in no rush) or far apart with less motivated Sellers (i.e baby boomers who bought their home for $300k and is now worth $1.8m but refuses it to be "undersold"). In my opinion, it's only a matter of time before people come around and accept the new norm. The market will find its footing and reach an equilibrium, and when the currently real estate sales is trending near all time low's, there is pretty much only one way it will go: up. Price may still be weak in the near future (at least 6 months), but sales will pick up. Such correction and cleansing are necessary. Also, lower prices means affordability is improving, even though it is still out of reach for many buyers.

On the national front, just when many thought the the Canadian government are starting to do something good (i.e Carney ramping up trade deals with Asian countries like India, China and Japan), what flew under the radar was that the government also further muddied the water by signing an acknowledgement of First Nation Musquem band recognizing the superiority of the aboriginal land title covering much of Metro Vancouver. Seems like the federal government can't help but to further gaslight the Vancouverites. These are some self-inflicted wounds that the government need to stop. Such agreement is neither helping with the images of the First Nations or the reconciliation, nor is it helping boost the confidence in investment in Canada. I wouldn't be surprised with seeing more capital fleeing the country as further land title disputes unfold. Oh, did I mention that not only is the Canadian public is in shock with agreement, but also OTHER First Nation bands such as the Squamish and the Tsawwassen bands are just as upset and is currently disputing the government's decision. When it comes to aboriginal land title disputes, the level of tone deaf the federal government has is really on another level. I am very interested to know what the government's game plan is moving forward, as it doesn't even seem like there is one at all.

On the global stage, the war in the Middle East has cast an even thicker cloud of uncertainty in an already unstable market. At the time of this writing, we are into the second week of oil supply disruption. From the looks of it, it doesn't look like this war will end anytime soon. Crude oil has jumped significantly and the stock market plummeted. With that in mind, we are staring down the eye of a global spike in inflation. Rising grocery prices are poised to be felt first and foremost, and this will hurt the middle and lower class the most. Heightened volatility causes bond traders to react, and so bond yields are trending upward, which means that fixed mortgage prices (which mirrors bond prices) are poised to shoot up as well. In other words, there would not be any lower fixed mortgage rates in the near future, as major banks are already baking higher rates into their forecast. Speaking of rates, the next Bank of Canada rate announcement will be on March 18th. General consensus will be no cut, but to road ahead will be met with yet another monumental task to whether hike or cut rates. The logic behind either decision is justified. On one hand, the Bank of Canada need to prevent the inflation from getting out of control, and so the need to raise rates would make the most sense. On the other hand, inflation compounded with a weak economy (aka stagflation) can be devastating, but can be somewhat alleviated in the form of lower rates (i.e lower mortgage payment) to save the average Canadian household. It seems like most bets are on the former choice, but with how fast things are going now (and it's only March), there's still could be a lot more surprises. Let's see.

Some of the unique trends I've been observing:

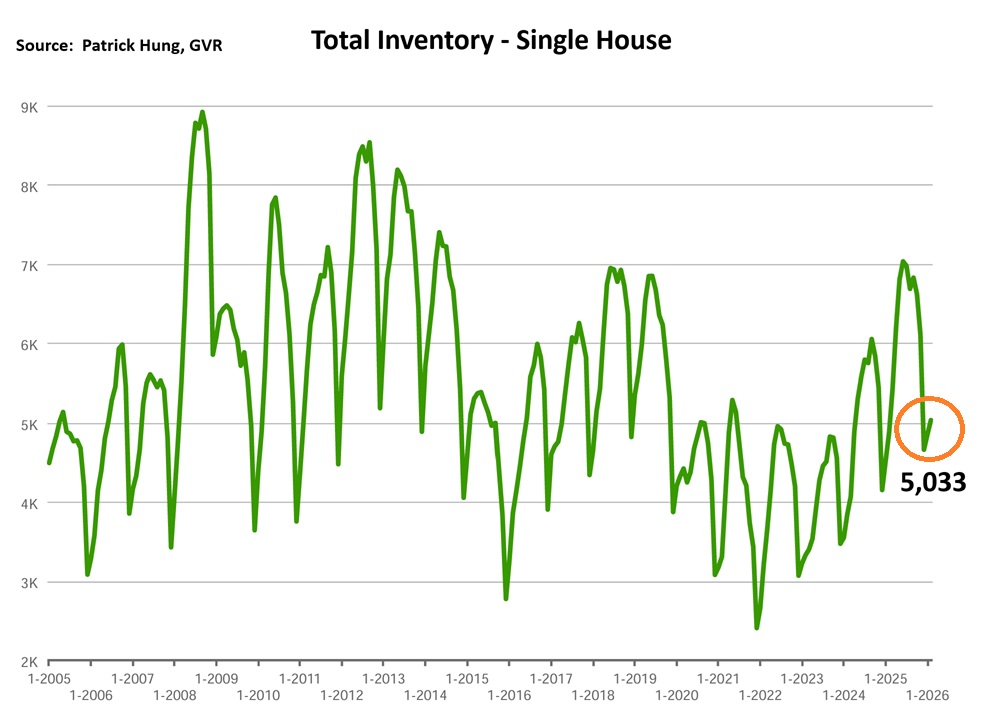

1. For the past 3 months, the Vancouver real estate market has been singing the same chorus of elevated inventory with lower sales. February had the 3rd slowest sale in the past 25 years, and to put it into perspective, there are 8.1 months of inventory now (5 months of inventory being a balanced market). Anecdotally, sharply priced homes are still attracting a lot of traffic, but Buyer confidence remain weak overall. Those who have been looking for the past few months may have finally come around as they now see the prices are falling within their comfortable range. March and April are typically the busiest months of the year, but with the war in the Middle East taking center stage, I wonder if that would further delay the plans of some Buyers.

2. The war in the Middle East is renewing fears of a fresh round of inflation, similar to that of 2022 of the war between Russia and Ukraine. Food inflation will be felt first and foremost, and the average middle and lower class will get hurt the most. It wasn't that long ago when beef and ground coffee had double digit jumps. Which ones are next?

3. With Vancouver real estate prices gradually declining to levels back to 2021-2022, the good news is that affordability is improving. What was different back then was that prices were ripping, bidding war happened every week, long lineup at open houses, and helicopter money is everywhere. Now, food inflation remains stubbornly high, unemployment rate is climbing, and more restaurants and businesses are closing. Even when the affordability stats are the same, the economic outlooks are very different.

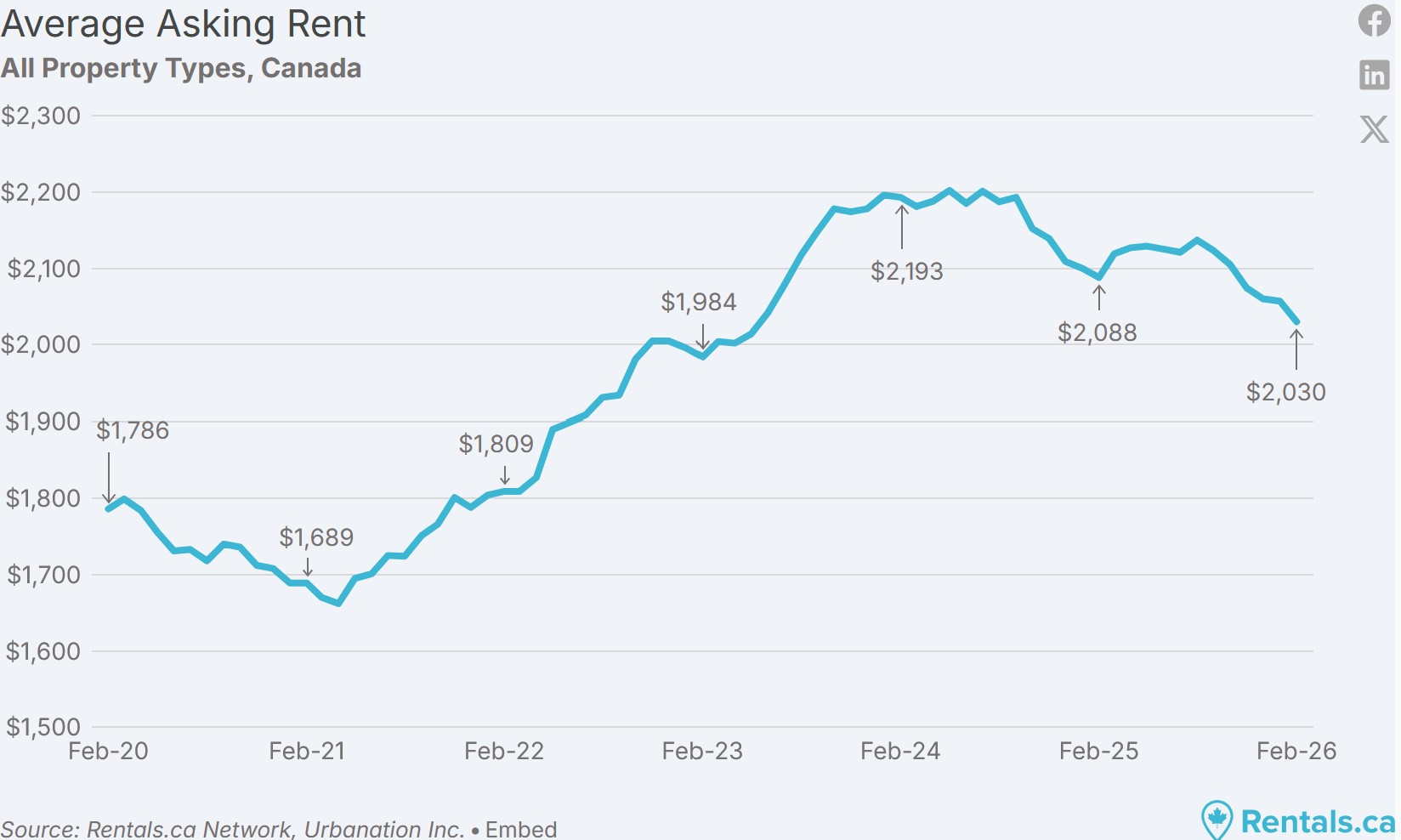

4. Rent in Canada have declined on an annual basis for the 17 consecutive month, as well as falling by 1.3% on a month to month basis, which is the largest decrease in February since 2020. Across all major provinces, Vancouver lead the charge in falling rent at -4.9%, followed by Ontario (-4.7%) and Alberta (-4.6%). With this in mind, retail investors continue to look away from real estate investments.

5. For the first time in a long time, the Vancouver real estate shifted to a balanced market (but still border lining a Buyers market), with sales-to-listing ratio (% of homes sold) is sitting at 12.6% in February, meaning only 12.6 out of 100 homes are sold, while the remaining 87.3 homes remain sitting on the market. This is an improvement from before, but I'm not overly convinced that the market has hit a bottom in terms of price. It will still take months of improved sales before prices start to flat line.

6. Canada's February unemployment rate shot up to 6.7% (from 6.5%) and lost a "surprising" 84,000 jobs. Digging deeper, there were 100,000 full time jobs that was lost. Youth workers aged 18-26 continue to take the hardest hit by losing 47,000 jobs last month. I was surprised how these numbers were published earlier, and the scary part is that we are witnessed even more business closures. Almost every week I'm hearing more restaurant closures, and business are either barely staying above water, or is going on hiring freeze. Can Canadian weather the storm of having rising unemployment at the same time with rapid inflation?

Here are the 3 highlights for February:

- Total inventory of 13,306 units is the fourth highest February's total inventory in the past 21 years. Sales are improving while inventory remains elevated. The gap between supply and demand is closing but only by a bit from previous months.

- After 3 months of consistently lower sales that's 30% below the 10 year average, some Seller seem to have finally got the message and come to their senses. Meanwhile, Buyers who have been window shopping for a while finally pulled the trigger.

- Benchmark home prices had a monthly price drop of -0.2% in February (compared to -1.2% in January). This brings the total of -2.1% price drop in the past 3 months. As new global conflict arises, it remains to be seen whether it would cripple the Buyers' confidence.

Here are the in-depth statistics of the February:

- Last month's sales were -28.7% below the 10 year February's sales average (compared to -30.9% in January). It is an improvement, but only slightly.

- Month by month residential home sales increased by +4.5% from January.

- Month by month new home listings dropped by -8.2%. This is normal due to the fact that January had many listings that expired in December and relisted in the New Year.

- Last month's price dropped further by -0.2% (compared to -1.2% in January)

- Sales-to-listing (or % of homes sold) ratio is increased significantly to 12.6% (compared to 9.1% in January). By property type, the ratio is 9% for single houses, 16.6% for townhouses, and 14.1% for condos.

Download February 2026 Greater Vancouver Real Estate Report

Single House Market

The single house market is sort of an outlier now in a sense of price, which was the only segment that registered price drop (-0.8%) compared to townhouse and condos (+0.2% and +0.5% respectively.) Months of inventory is also the highest amongst all property types, sitting at a whopping 11.8 months (for context, 5 months is a balanced market). In other words, single house market have double of the supply of a healthy market. Even when the price are falling within the comfort zones of most buyers, there is just a lot of supply for them to choose from, so the element of time is still favoring the Buyers. What we did notice though is that, since the new year, single house Sellers are more willing to reduce their prices or to list their home at a competitive price. There are pockets of neigborhood in the prestigious in Vancouver such as Shaughnessy, South Granville and Arbutus, with multi-million dollar homes at a sales ratio of 4%, 5%, and 7% respectively. This means only 4-7 homes out of 100 are sold, where 93-96 of them are sitting. The downward price pressure is mounting and Sellers see that. Of course, real estate is hyper local and there are also neighborhoods such as Coquitlam and and North Vancouver (with sales to listing ratio between 14%-20%) that are faring much better than others areas such as Richmond and Port Moody (with sales to listing ratio between 6-8%). Anecdotally, entry level single house are still in high demand and is attracting decent traffic, with the occasion ones that are selling quickly within 2 weeks, or a rare one that was listed under market price for bidding but end of up selling fairly close to market price. Again, partial of the increased traffic can be attributed to seasonality, with Spring being the busiest season. However, one may argue that the single house Buyers are still circling around, but just being extremely selective with their choices. As Buyers and Sellers clearly see that inventory is plentiful, only the most best listings with competitive pricing, ideal location, practical layout and in move-in condition (no renovations required) are the ones that sell quick. But the thing is, there is just not a whole lot of these on the market now. Then again, there will always be unrealistic single house Sellers who bought their home 20 years ago for $500k (which is now worth $1.8m) and wants to sell at a highest price, despite their average condition home. As Spring is around the corner, which is the busiest time of the season with the most homes coming onto the market, we should see more and more "good" listings. But the scary part is that good listings will become the standard expectation of the Buyers, and only the BEST listings will sell.

For the month of February, the neighorhoods that registered most price growth were Whistler, Squamish, and Burnaby East, posting +2.2%, +1.8% and +1% respectively. Conversely, the neighborhoods registered the most significant price drops were Tsawwassen, Burnaby North and Coquitlam, with -3.2% (tied for 1st and 2nd) and -2.2% respectively. The single house market remained in the Buyers market, with average days on market improved to 49 days (compared to 61 days in January), and month-to-month average price declined by -0.8% (compared to -1.5% in January). Sales-to-listing ratio (% of homes sold) increased to 9% (compared to 6.7% in January).

Townhouse Market

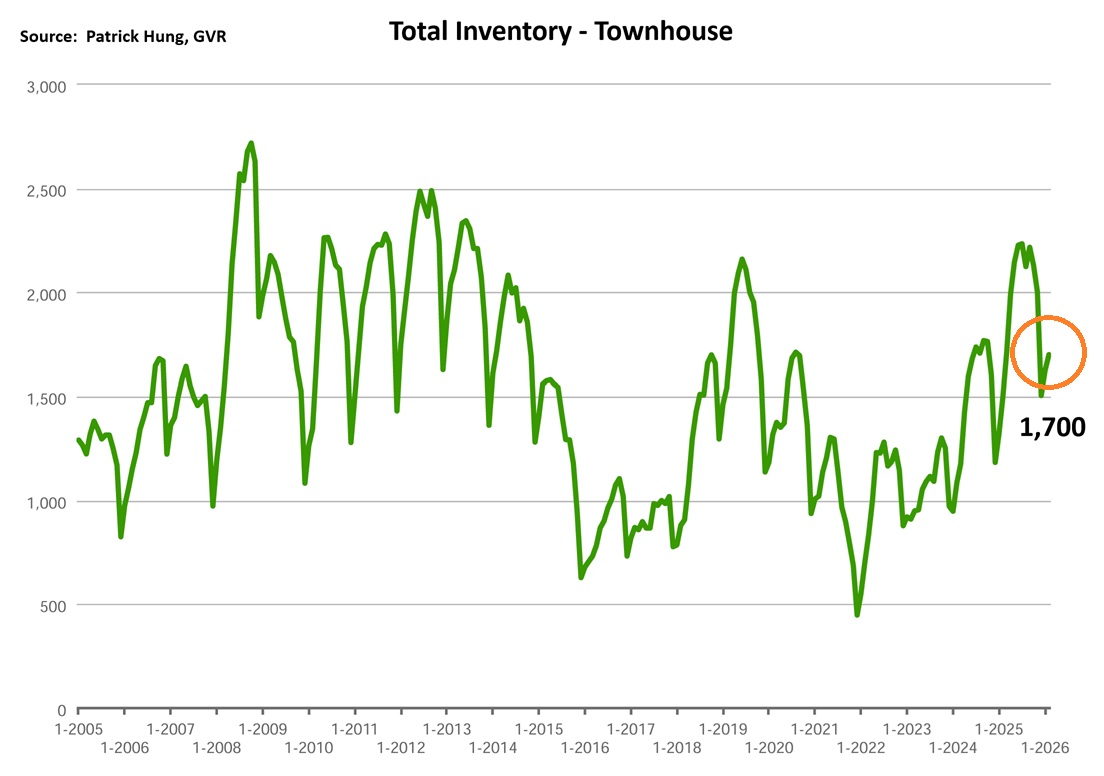

For the past month, townhouse market was again caught right in the middle, with modest price gain of +0.2%. Key is that the months of inventory has fallen to 5.8 months (for context, 5 months is balanced market), so for this segment we are starting to see a return to a normal market. Anecdotally, we are seeing some townhouse prices fall closer to that of a newer 2 bedroom condo. This makes the upsizing buyers (i.e family who just had another child and is looking for more space) that much easier to transition. On top of that, townhouse also enjoyed the best sales-to-listing ratio (% of homes sold) at 16.6% across all segments. One of the competitors in the townhouse market is the new type of home: the multi-plex with 3 or 4 units under one roof. Such multi-plexes are much more competitively priced in terms of price per square feet, and also do not require paying a monthly strata fee. The biggest drawback, though, on the multi-plexes is the parking issue, where 4 units may only have 3 open parking, with no enclose garage (safety). Such parking issue will be common across Vancouver as more and more of these multi-plexes come into play, and that is where townhouses have a leg up on its competitors. Anecdotally, Buyers are now comparing hard between these two types of properties as both townhouses and multi-plexes see sales rise with a lowered inventory base. I'm actually grateful that more multi-plexes are built and is providing more options for Buyers, as this is sorely needed to meet the needs of the middle class and growing families. For the same reason, I wouldn't be surprised if the townhouse market (and multi-plexes) continue to outperform other segments: the recovery of the townhouse market may come sooner than expected due to its relative affordability and practicality.

In February, the areas with the most townhouse price growths were Tsawwassen, Ladner and Vancouver West, registering +3.9%, +2.5%, and +1.9% respectively. Conversely, the neighborhoods with the most significant price drops were all out in the outskirts in Sunshine Coast, Squamish, and Whistler at -2.9%, -2.5% and -1.3% respectively. The townhouse market has quickly shifted from a Buyers market into a Balanced Market, with days on market dropping to 33 days (compared to 37 days in January). Month-to-month sale price has finally posted a gain of +0.2% (compared to -1.2% in January). Sale-to-listing (% homes sold) ratio also shot up significantly to 16.1% (compared to 11.1% in January).

Condo Market

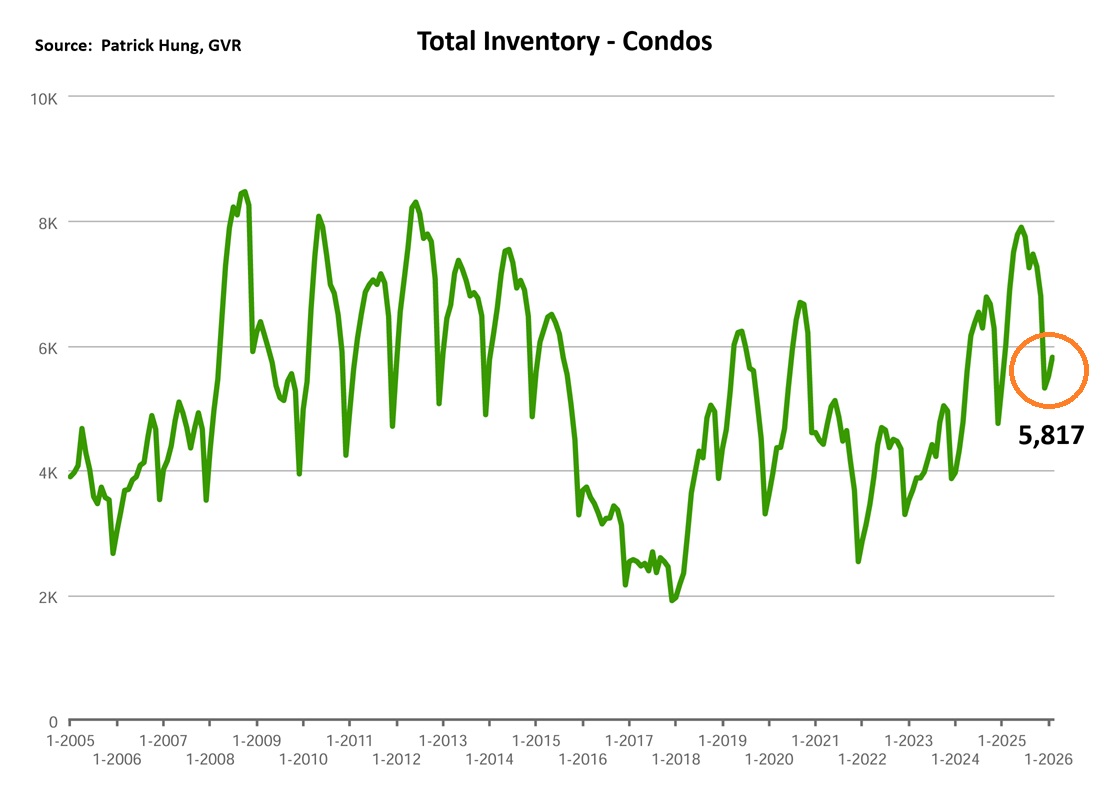

In terms of price, the condo market is showing signs of rebounding, from a 3 months price change of -0.9% compared to townhouse (-1.8%) and single house (3.4%). Last month, it continued that trend with the highest price jump in recent months at +0.5%. Could this be a a sign of recovery or a blip on the map? While it is definitely a pleasant change of winds, I still think it's too early to tell. On the supply side in 2026 and early 2027, Greater Vancouver (especially Fraser Valley like Surrey and Langley) will have plenty of completion of pre-sales, and such projects will have hundreds and thousands of new homeowners, with many investors who are looking to liquidate. In the short term, we are seeing condo prices come down to a point where supply is comfortably meeting demand and has returned to a balanced market, with sales-to-listing ratio (% of homes sold) at 14.1%. Some first time home buyers, whom have been waiting for the past 3-6 months, are finally pulling the trigger as the price of their ideal home is making sense. However, retail investors are still nowhere to be seen as pre-sale market collapses. There will be a window in approximate 3-4 years where there will be hardly any condo/apartment new constructions, and will very likely cause a limited supply (if immigration returns). With that, price may be driven up. However, the current condo market feels like the oversupply are highly concentrated in the Fraser Valley area (i.e Surrey, Langley), whereas traditionally scarcely supplied area like Vancouver West (balanced market) and North Vancouver (Seller's market) are seeing a much different story. The side story that feeds into the condo market is the return to office mandate that was implemented Q3 of 2025. This has caused many young professional working in Downtown to return to Metro Vancouver, and is considering purchasing somewhere closer to work. For this reason, condos in the downtown area along with Vancouver Westside and Eastside are making a slight comeback with higher sales-to-listing ratios. However, communities that require further commute (like Fraser Valley) are still sluggish.

For the month of February, the best performing neighbourhoods for condos were in Squamish, West Vancouver, and Sunshine Coast, at +3.6%, +3% and +2.6% respectively. Conversely, the areas with the most significant price drops were mainly in Tsawwassen, Ladner and Burnaby East, posting -3.5%, -2.7% and -2.6% respectively. The condo segment shifted into from a Buyers market to a Balanced market, with average days on market dropping slightly to 40 days (compared to 49 days in January). Month-to-month sale price reversed back to the positive at +0.5% (compared to -0.8% in January). Sale-to-listing (% homes sold) ratio increased significantly to 14.1% (compared to 10.3% in January).

1. Suicide Squad

Just when Canadians are starting to forget about the First Nation land claim a few months ago, the federal government has decided to gaslight the entire BC homeowner base by agreeing and recognizing the Musqueam First Nation's aboringal land title. This means that Musqueam land title will be SUPERIOR to the private land title covering nearly all of Metro Vancouver. There are so many things wrong with this. Firstly, why was there no public inquiry before a huge decision like this was made? Secondly, even other First Nation bands such as Squamish and Tsawwassen were infuriated and has appealed the decision. So not only is the BC NDP government on a suicide mission, but so is the federal government. Worst part is, this was all done in secrecy and nobody found out until it's signed and sealed. (Source: DailyHive.com)

2. Higher Everything

In developed countries, oil price trickles into everything. As crude oil hoovers around US $100 per barrel (March 13), there is no sugar coating the imminent spike in inflation. For this exact reason, traders of the bond yields react, causing bond prices to go up. As such, mortgage rates mirror that of the bond rates, and so we are starting to see the fixed rates (not variable rates) have climbed to the highest point in 2026. Some mortgage specialist project 5 year fixed rates will be above 4% very soon. For those who are looking, perhaps it is wise to consider locking in your rates to avoid further upward swings. (Source: Investing.com)

3. 17 Going 18

Rent in Canada has fallen on an annual basis for the 17 consecutive month, as well as falling by 1.3% on a month to month basis, which is the largest drop in February since 2020. The most populated provinces felt it the most, such as Vancouver (-4.9%), Ontario (-4.9%) and Alberta (-4.6%). The long road to rental recovery remain elusive for now. (Source: Rentals.ca)

Recent Posts

GET MORE INFORMATION